Reshaping a Broken Industrial Robot Market: Introducing the Era of Physical AI + Robotics as a Service with Verne

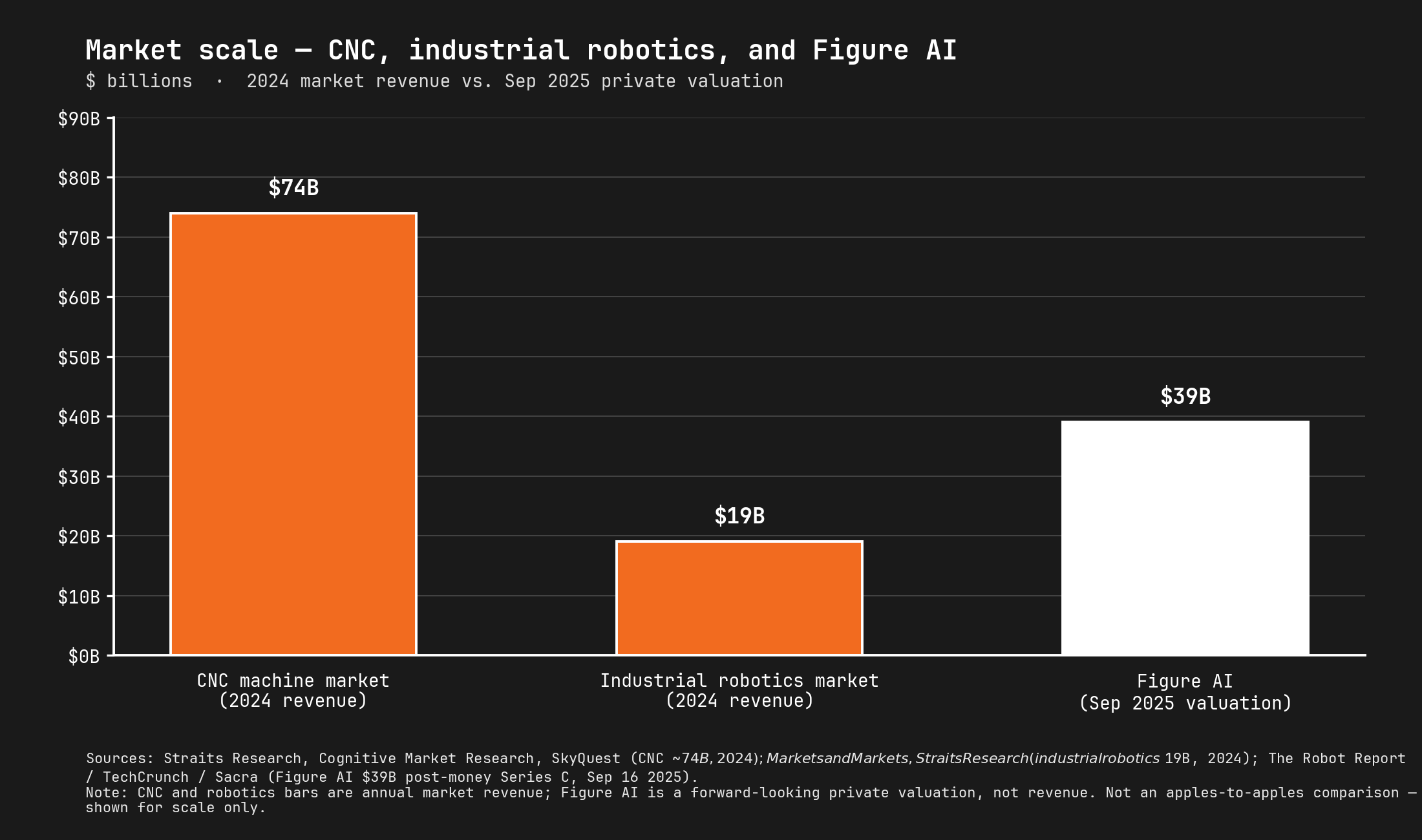

If I held a gun to your head and asked you to guess the market value of a century-old industry that out-precisions human laborers by a factor of five and has reduced manufacturing injuries by more than 60 percent, you would probably guess something massive. Industrial robotics is only worth roughly ~$20 billion (Estimates vary by source; this is the ballpark). This is less than a single humanoid robot company’s valuation (that has sold zero robots to the general public). A quarter the size of the CNC machine market.

This essay explores why that gap exists, and why it is finally closing. For a century, every industrial robot ever deployed has been a single-purpose machine. They are engineered for one task, in one cell, with months of system integration time. That constraint is what made the economics of robotics forbidding (high capex, long deployment, multi-year lock-in) and what kept the customer pool so small that only a handful of industries (automotive, electronics) could afford to play. Both halves of that problem - the limited generalization of robots and the economics built around deploying them - are now being solved. Physical AI breakthroughs enable general-purpose robots that can be re-tasked by feeding the system new data rather than re-engineering the machine. And a new business model, Robots as a Service, introduces vertically integrated providers to strip out the capex and integration burdens that priced everyone else out. Verne is delivering physical AI + Robotics as a Service via general-purpose hardware and AI models, with embedded operations and financing.

A Short History on Industrial Robotics

Industrial robots spawned into existence in 1930 via a very simple pick and place crane at the time. From there, the industry developed as man’s ability to control industrial robots via computer systems did, with the hallmark growth points arriving via:

The 1966 release of the Unimation computer controlled Unimate 1900 (famously adopted early by General Motors)

The 1969 release of the first robotic arm, The Stanford Arm

The 1980s-90s progress in industrial lasers enablement of sensor technology and further computer control via 1994s multi-robot control

The 2010s revolutionary advancement of human-robot collaboration and automation

The Physical AI Era - Achieving Faster Programming

The history above is one lineage: robots learning to move precisely along pre-programmed paths. A second lineage matters just as much - intelligence, the ability to handle a world the robot wasn’t explicitly programmed for. A 2015 industrial robot could weld a car door ten million times in a row, but ask it to pick a slightly different part from a slightly different bin and the system collapsed. This, more than anything, is why robots are absent from almost every workplace you’ve ever set foot in.

The clearest demonstration of this lack of generalization came from the Amazon Picking Challenge launched in 2015. The task was simple: build a robot that can pick arbitrary consumer items off a warehouse shelf. The world’s strongest robotics labs - MIT, Berkeley, TU Delft - entered. The 2016 winner, Team Delft, topped out at roughly 100 picks per hour with a 17% failure rate. That was the best result on Earth on a simplified version of warehouse work. Underwhelming at best. The two dominant paradigms of the era, rule-based control and computer-vision pipelines, simply could not handle a warehouse shelf. They were never going to handle a factory floor that wasn’t already custom-built around the robots. This is exactly why, for decades, the only sectors with robots deployed at scale were the ones that could afford to build their floors around them such as automotive and electronics. Everyone else was priced out.

From Rules to Learning

Rule-based robotics, the first wave to smarter robots, ran on hand-engineered rules written by a system integrator who had to anticipate every condition the robot might face. They worked beautifully in environments that never changed and broke immediately in environments that did. Traditional industrial robots live inside fenced cells for a reason: the cell exists because the software cannot generalize beyond it.

The second wave, computer vision, gave robots eyes. Deep learning made scene understanding possible and for the first time a robot could see a cluttered bin (side note: we are very excited about and pursuing more advanced sensor technology to 1000x the useful data generated by sensors to improve all systems including robotics). But seeing is not doing. Perception and action remained separate stages connected through brittle interfaces. The robot could perceive and describe a messy world. It still couldn’t act in one. Contact-rich assembly, deformable objects, grasping in clutter were simple tasks still out of reach.

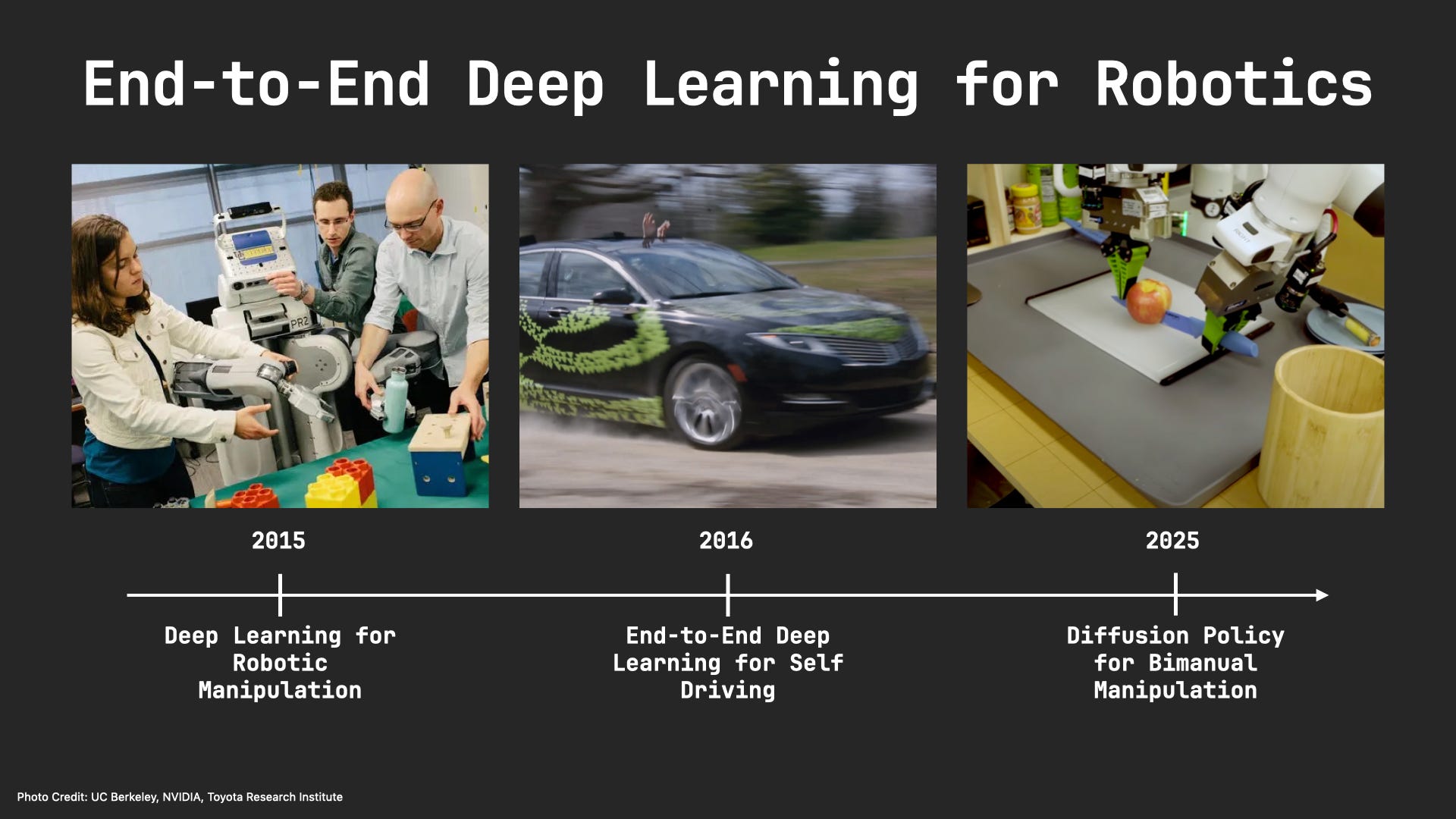

The true unlock was end-to-end policy learning, first commercialized in 2024: pixels in, actions out. A single neural network maps raw sensor input directly to motor commands. The analogy is Tesla’s full self-driving stack, where rules were replaced by a learned model. In 2023, Shuran Song’s lab (then at Columbia, now at Stanford) published Diffusion Policy, an approach that showed end-to-end deep learning could match or beat the best hand-engineered robots on manipulation tasks. None of this was possible five years earlier. (Another side bar: we continue to actively explore multi modal models that can model the physical world, such as diffusion).

What emerges is something new: a robot taught a task in an afternoon instead of programmed for six weeks. The fence around the work cell is no longer required. The list of industries that can actually use a robot is no longer capped at the few that could afford the integration. This is the substrate underneath everything Verne is building.

The capability bottleneck that kept robots absent from the real world for a century is shrinking fast. But adoption has barely moved. Whatever is still holding industrial robotics back is not just the intelligence of the robots.

Proving Adoption Failure By The Numbers

Despite these advancements, the increasingly lower price per robot and the clear potential benefit of automating processes, the adoption of industrial robots is still much lower than one would expect. Consider:

The use of industrial robots is highly concentrated. 65-75% of the market is dominated by automotive, electronics and machinery.

The use of industrial robots is also highly concentrated. Nearly three-quarters of all robots operate in just four industrial groupings: computers and electronic products; electrical equipment, appliances, and components; transportation equipment; and machinery.

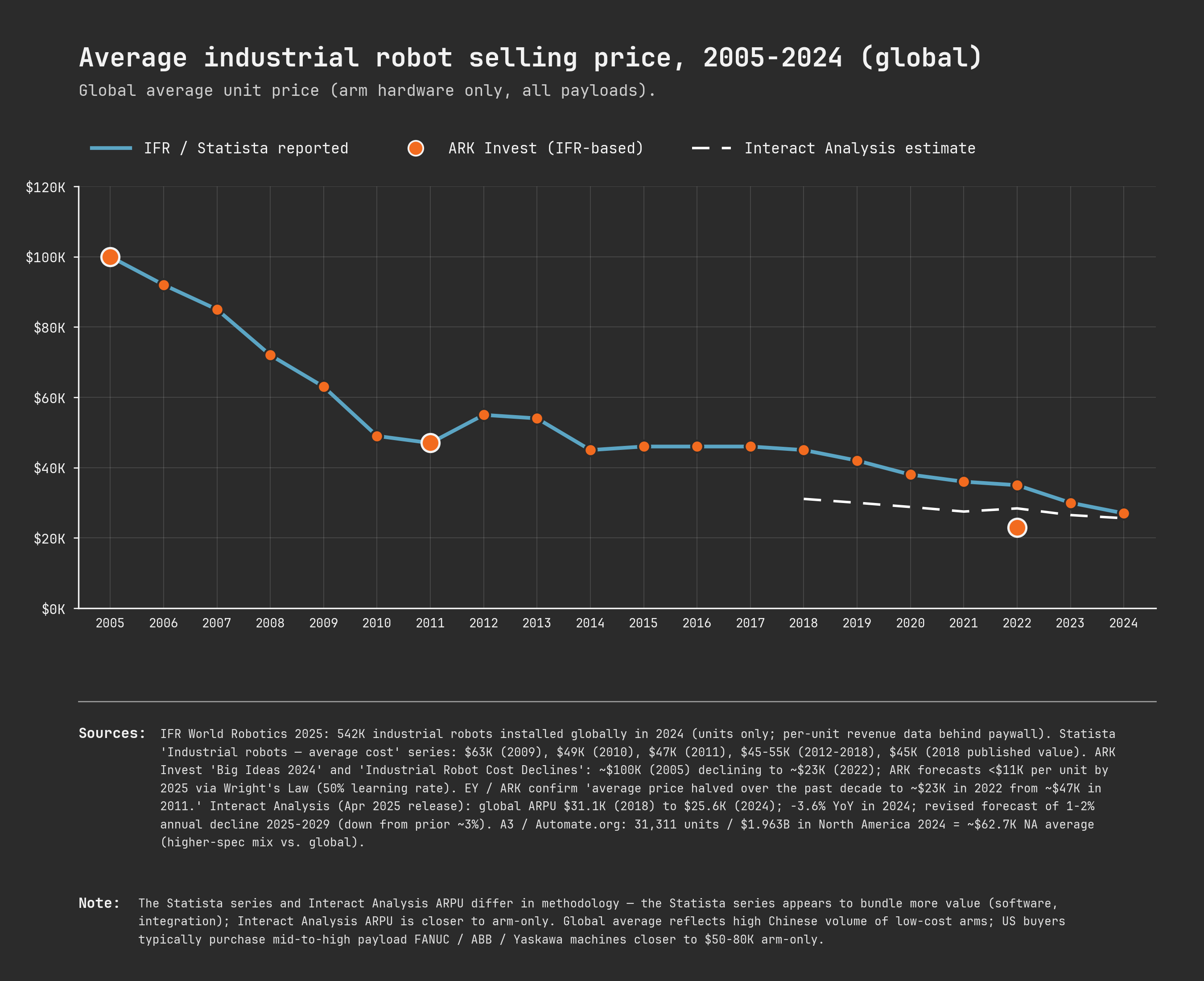

The size of the industrial robotics industry, as a result, is estimated between $18b and $55b depending on the data source. This is at most 25% the size of the CNC machine market.

One must ask: why have industrial robots failed to become more pervasive in industrial systems? The answer we’ll offer is the fundamental structure of the robotic economy.

The Real Cost of Deploying a Robot

If intelligence is no longer the bottleneck, the rest of the answer has to live in the economics of getting a robot onto a customer’s floor - and that math is harder than most people realize. Deploying an industrial robot involves several non-trivial operational and economic processes and decisions. Let’s walk through them by component:

Pre-Deployment Planning & Site Preparation: significant groundwork is required - requiring a system integrator to implement safeguarding, control interconnections, task specific programming, creation of a Risk Assessment Method Statement (RAMS), and risk assessments.

A realistic budget must account for the fact that the robot arm is often only 25-50% of total project cost. The budget must also include end-of-arm tooling, safety equipment, installation and commissioning fees, integration software and engineering, training expenses, and ongoing maintenance and spare parts.

Physical Installation and Commissioning: installation is a robust process involving installing and leveling the robot base, verifying anchor bolt torque specs, connecting electrical and network services, loading applications, executing the SAT protocol. This is a multi day process.

Controlling & Operating: Each major manufacturer runs a proprietary OS and programming language that are not fungible with those of other manufacturers. A company implementing a robot from a specific manufacturer is making a multi year commitment, innately, to their manufacturers systems, networks, programming languages, etc.

Operator Training and Handover: complex industrial systems require approximately $10,000 per operator for one week of formal training.

Ongoing Maintenance: Annual robot maintenance costs 5-15% of the original purchase price, averaging $3,000-$15,000 per robot per year plus unplanned downtime. Estimates show the total cost of ownership (TCO) across a 10-15 year lifespan is typically three to five times the initial robot purchase price.

Payment Structures: the vast majority of industrial robotics transactions today are either:

Funded with 100% capex at $50-80k per robot before installation and ongoing maintenance and opex costs.

Leased: a $45k robotic arm rents for a few $k per month depending on the lease structure.

Taking all of that into account, deploying an industrial robot, while at face sounds like +ROI, is in reality a heavy operational, logistical, and financial burden. Most of that cost is not about the robot itself but rather it’s the per-deployment integration work around it. That cost curve has kept the robotics industry small for a century, and it’s about to change.

“Software Is Eating the World”. Robots Are Next.

Robots are about to undergo what software underwent over the past 30 years: a shift from artisanal, per-project economics to amortized R&D delivered as product. Physical AI and a new business model are the enablers of this progression.

For a century, every industrial robot has lived in the system integration cost shape. The customer pays in full for a custom-engineered intelligence layer: task programs, cell logic, bespoke tooling, integrator hours. There is nothing to amortize because every deployment is its own R&D project. The arm could come down in price all it wanted, and the surrounding work wouldn’t.

Software, by contrast, has had the right cost shape for decades. Best-in-class SaaS clears 80-85% gross margins; one more user opening Slack costs almost nothing to serve. But that story has always been partial. Even pure SaaS typically derives around 15% of revenue from professional services, and Palantir popularized forward-deployed engineering because enterprise customers need highly embedded work to ship the product. The AI wave is bending the curve further: modern AI deployments look more like a forward-deployed layer on top of an enormously expensive trained model than they look like classic SaaS. The honest shape of the modern software economy is not “zero marginal cost.” It is “heavy R&D amortized over time, with a bounded forward-deployed layer per customer.” Still categorically different from system integration.

Physical AI moves robotics into the same family. A physical AI model trained on millions of hours of real world data lets the marginal customer access an enormous, shared, continuously improving capability for a fraction of what it would cost to build alone. The R&D is paid once. The capability is delivered everywhere, with a bounded forward-deploy layer per customer. Robotics will never reach per-seat SaaS economics - robots are physical, and physical things cost real money to build, install, and maintain. But the value isn’t necessarily in the margin. It’s in what physical AI eliminates: per-customer system integration, historically the single most expensive line item in any robot deployment.

But cost structure alone isn’t enough. The technology has to come paired with a business model that makes it accessible to customers who can’t build it themselves. AWS is a great example. Cloud computing existed for a decade before AWS, sold by Sun and IBM as “grid computing” to almost nobody. What Amazon shipped in the mid 2000s was a new business model of utility pricing, self-serve API, no contract, no salesperson. Within a decade every company in tech was building on it. Sun’s grid-computing customers in 2005 were mostly Fortune 100 IT departments. AWS made the same underlying capability accessible to startups. Same technology, sold differently, opened a market a thousand times larger.

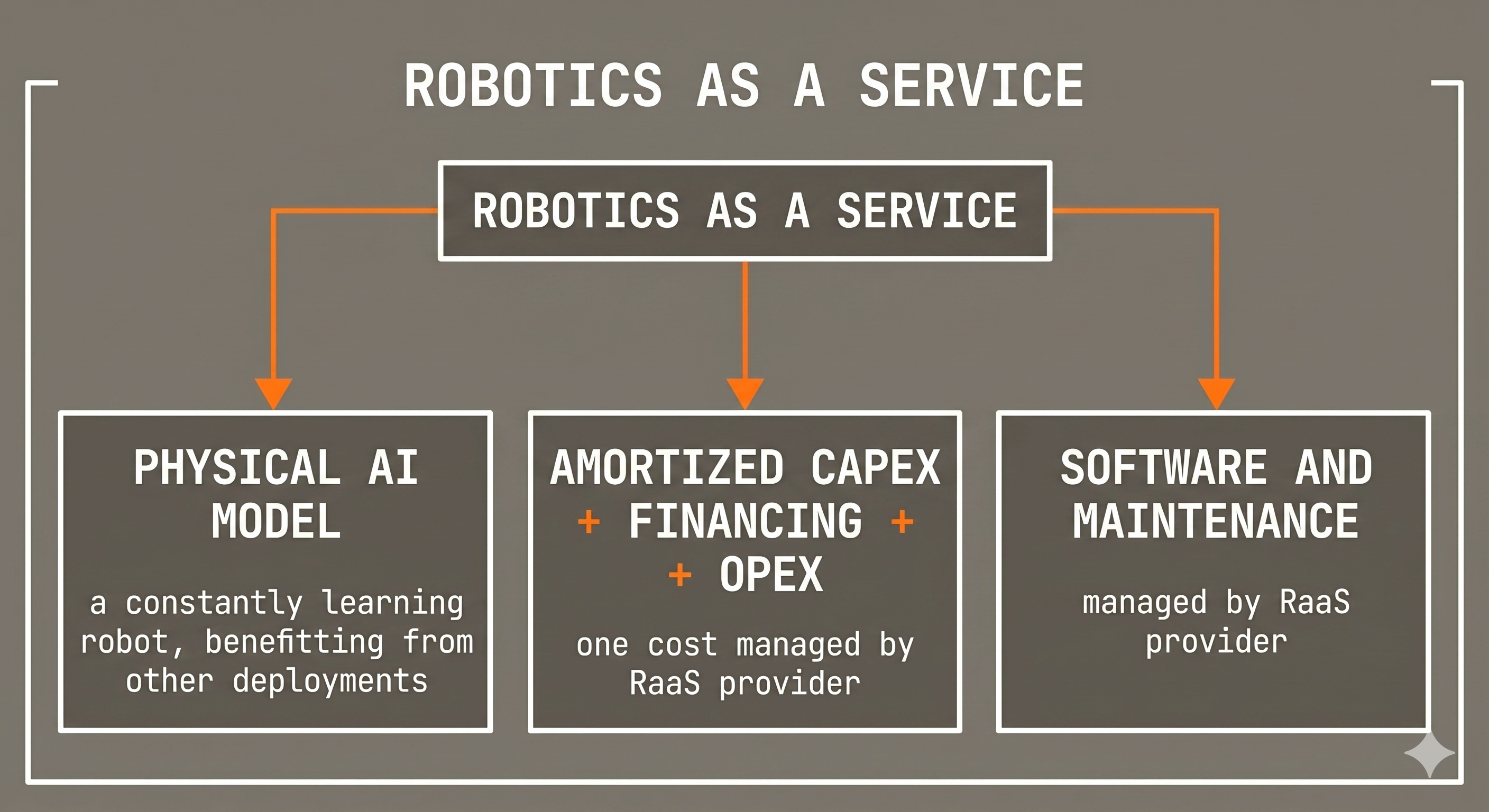

Robots as a Service

That is the shape of the robotics platform shift now arriving. Physical AI is the technology. Robots as a Service is the business model. The customers who have been priced out of robotics for fifty years are not the existing Fortune 500 but the tens of thousands of small and medium enterprises that comprise America’s industrial base. Same physical AI stack, delivered differently, opening a market that has never existed.

Every platform shift takes two inventions: a technology that makes something possible, and a business model that makes it usable. One without the other is a research paper.

A new ecosystem is forming around this unlock, and we welcome all of it. Foundation-model labs like Physical Intelligence, Skild, and Generalist are training the general-purpose brain. Hardware companies like Standard Bots and Neura Robotics are building next-generation arms. Vertically integrated players like Formic are deploying within narrow verticals. Others like Machina Labs and Bright Machines are bringing more intelligence to specific manufacturing use cases. Each of these matters. None of them, on their own, directly and completely address the core barriers to industrial robotics adoption: the capex burden and the operational complexity that surrounds every deployment.

Robots as a Service (RaaS) is the business model that finally fits. No capex upfront, costs embedded into a monthly lease, and a specialized operator handling financing, deployment, and maintenance end to end. The subscription only works because physical AI has changed the economics underneath it. A general-purpose model trained on millions of hours of real-world data can be retasked across customers, which means the R&D is amortized across an entire fleet instead of rebuilt for every deployment. A single robot on a Verne lease gives the customer access to a continuously improving model trained on the cumulative experience of every other robot in the field. That kind of capability used to require a Fortune 500 integration budget. Now it fits inside a monthly line item. The honest comparison isn’t RaaS versus owning a robot - most of these companies were never going to own one. It’s RaaS versus paying humans to do the same work, where humans still work eight-hour shifts and a Verne robot works 24/7 at a fraction of the variable cost.

The Endgame is Fully Integrated RaaS + Physical AI - Introducing Verne

Industrial robotics is undergoing two simultaneous breakthroughs: physical AI on the capability side, Robots as a Service on the access side.

A new generation of companies is forming around the unlock. Foundation-model labs are training the brains. Data providers are appearing to feed those models the robot data the internet doesn't contain. A small number of operators are deploying robots into customer sites. Capital partners are starting to underwrite robot fleets the way utilities are underwritten: against the cash flow of the work itself. The endgame is clear, even if most of the industry hasn't yet said it out loud. Within a decade, the way work gets done across America's industrial base will be transformed by robot labor that learns. Every factory floor, every kitting line, every back-of-house operation will run on fleets of general-purpose robots - financed like infrastructure, operated as a service, improving every week from the data they collect. This is what an industry looks like in the year before that endgame becomes obvious.

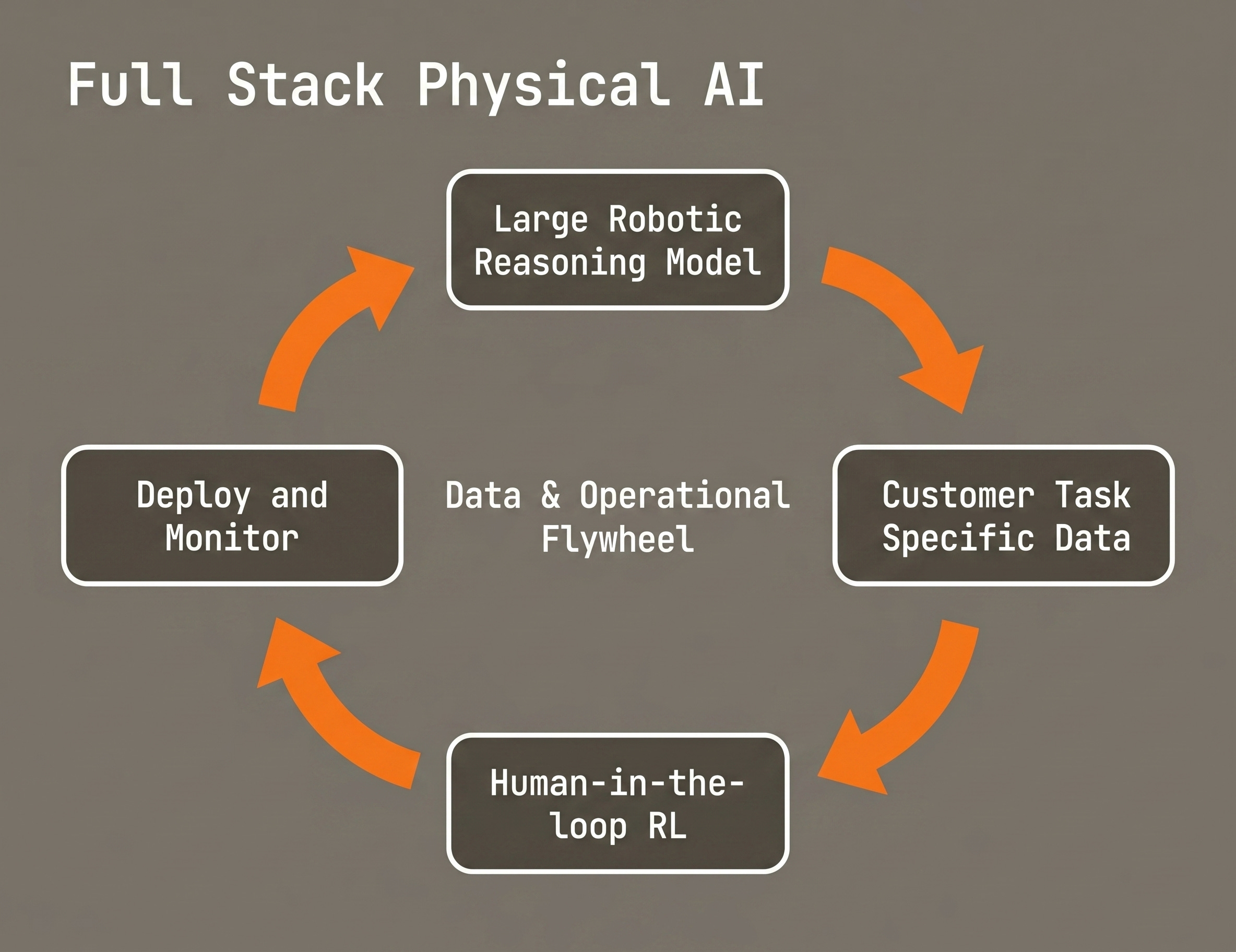

Most of these players will pick one layer and try to win it. A few will own the vertical stack from model to hardware management to financing. The argument for owning the stack is both necessary and practical. The capability gains in physical AI come from a single loop: collect data with the same hardware the robot will use, train a model tuned to that hardware’s geometry, deploy it onto a fleet, watch where it fails, retrain. The loop only compounds if one team controls every step. Model labs without fleets train on someone else’s distribution. Fleet operators running someone else’s model can’t fix what scale exposes. Hardware vendors without a model have nothing to amortize R&D against.

Verne is taking a different approach, vertically integrating the entire physical AI stack - from data to model to financing to deployment. The work holding most businesses back is high-mix and dexterous - medical kitting, food processing, mixed-SKU pick and pack - the messy middle traditional robotics can’t touch and physical AI now can. The Fortune 500 already has robots. The middle of the American industrial base never has. We walk into a customer site, collect under five hours of task-specific data with our hand-held grippers, and have a robot working on their floor in under a week. The customer watches it improve at their specific work week over week.

The industrial robotics market has been stuck at twenty billion dollars for a generation. Over the next decade, it pushes into the hundreds of billions. We believe every business in America deserves a robot. We believe that robot should be a Verne robot.

| A guest post by

|

| A guest post by

|