Understanding the Nuclear Fuel Value Chain

Building American energy independence one isotope at a time

Note: this report was modified from its original version to fit this Substack. For the full formatted version, including footnotes and additional graphics, please see

Intro - No More Shiny Objects

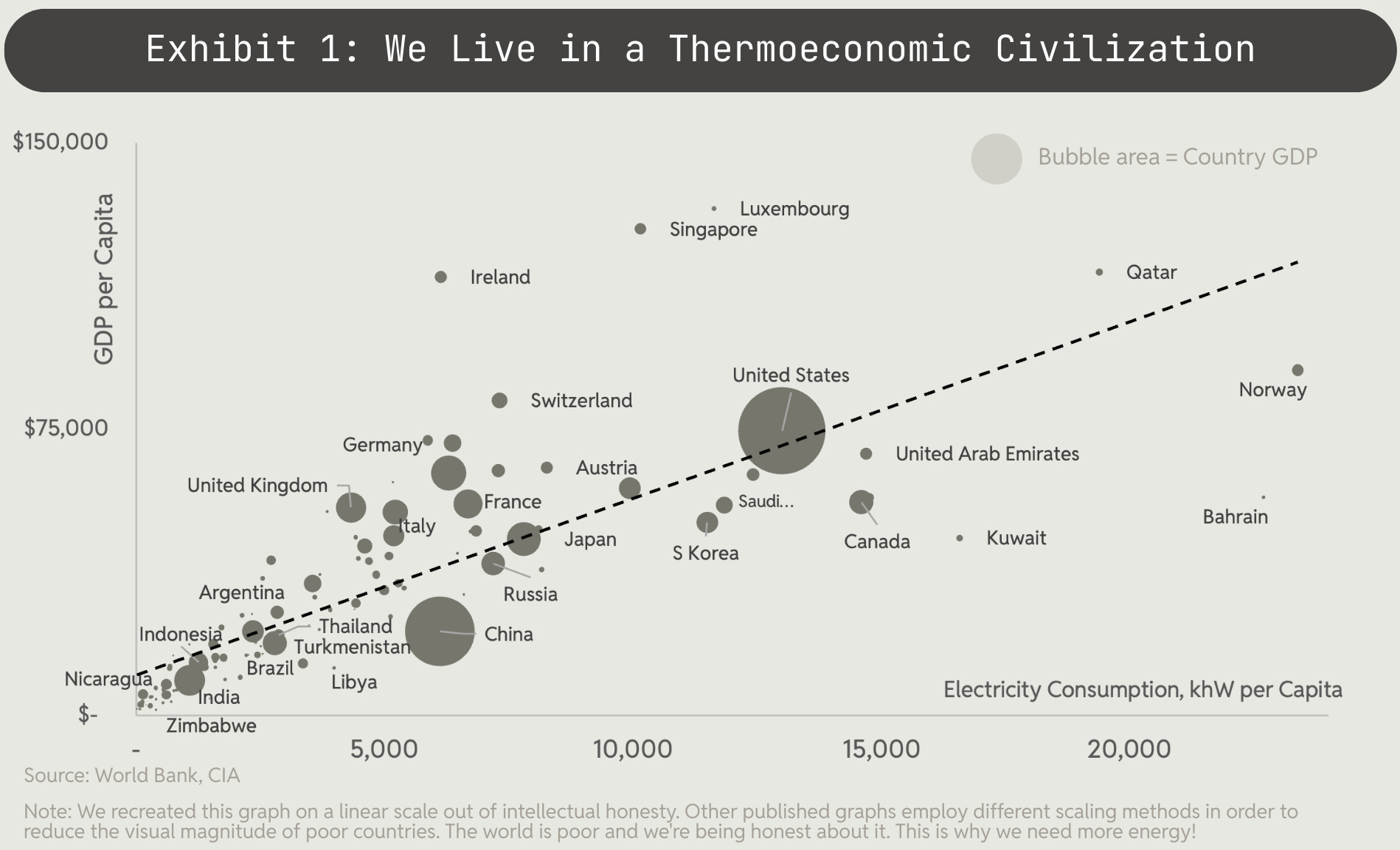

The more energy a civilization consumes the more it prospers. The relationship between national per capita energy consumption and per capita GDP is irrefutable. For the last fifty years, the global energy economy ground to a halt as aging hippies and ESG initiatives pushed Malthusian rhetoric and curtailed infrastructure investment.

Bitcoin took the brunt of the ESG ire but ultimately built the playbook for today’s high

performance data centers - co-locating energy generation and compute to take

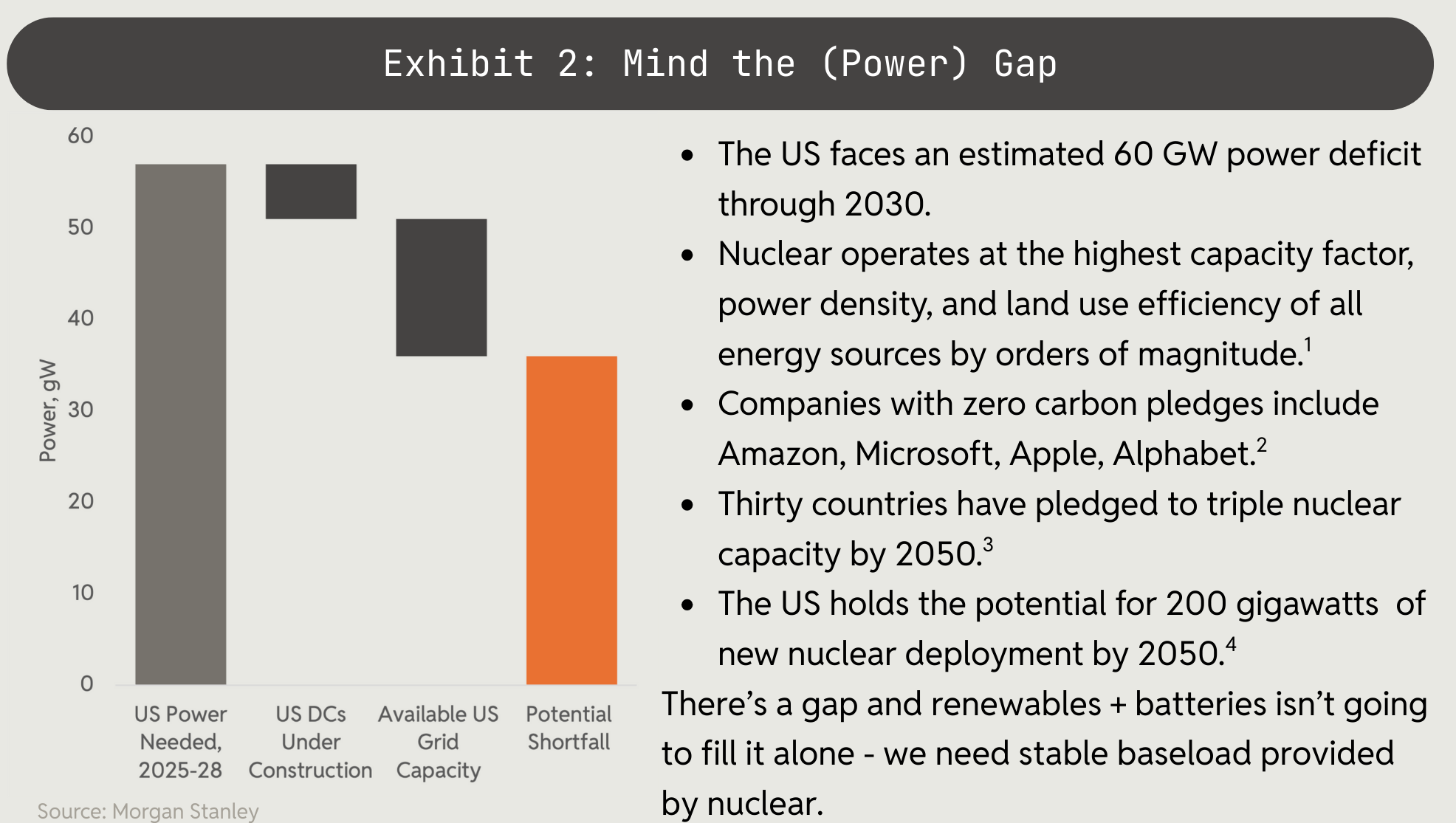

advantage of excess power both on the grid and behind the meter. It took the demand of the Magnificent Seven seeking to build gigawatts of compute infrastructure to wake US investors and policy makers up to the necessity of energy abundance, but attention is finally being paid to harnessing the power sources in our reach to fill America’s gaping power deficit in the coming years (Exhibit 2). With power stability, density, and emissions in mind, we’re finally scrapping our long held false inhibitions about nuclear power - the densest source of 24/7 baseload power known to mankind. Nuclear isn’t just about more generation on-grid, but also about delivering power density and Kardeshev Scale advancement - this technology is foundational to humanity’s arc of progress.

We won’t justify one power form over another here - we need all sources to meet the parabolic rise in demand - and all forms of power production excite us at Crucible.

(except for Thorium, we don’t like you Thorium, you can’t sit with us. You are ugly and don’t have high cheekbones like us. You don’t even compete athletically or intellectually. Bye, Thorium, don’t hate me because I’m beautiful. Also don’t even get us started on metal fuel. Ok we’ll stop now.)

We won’t spend time in this report preaching the gospel of nuclear either - many have laid this foundation already. Instead, we will shift from aspirational rhetoric to real blocking and tackling on how we will get there by focusing on the most underinvested aspect of the nuclear renaissance - the fuel needed to power it.

In order to invest effectively, we have to zoom out and look at the value chains that

emerging new technologies will depend on. Our firm is named Crucible in honor of the high purity quartz mined at Spruce Pine, NC to make the crucibles needed to forge silicon ingots - the linchpin underlying the global semiconductor value chain. No high purity quartz, no crucibles, no silicon ingots, no semiconductor industry, no compute. The inability to understand value chains leads to misallocation of capital, and these misallocations persist all throughout the deep tech landscape - we are investing in futuristic cars and vehicles to speculate on the price of futuristic gasoline without investing in procurement of gasoline itself.

The US has underinvested in the nuclear fuel cycle since the 1970s due to its own

regulatory missteps which is ironic considering the industry was born out of government research in the 1940s. The US instead chose to rely on Russian imports, leaving us in a vulnerable position as global trade wars and embargoes flare. The fuel cycle, from yellowcake U3O8 to converted, enriched and fabricated fuel, is fragmented and complex, and yet it’s crucial that we understand these complexities in order to secure durable domestic nuclear fuel supply chains in the coming years - as a matter of both economic and national security interests. This is exacerbated by the fact that the advanced reactors that are sucking up the misallocated capital use different forms of fabricated fuel, the most prominent form being TRISO (tri-structural isotropic) fuel, whose manufacturing is fundamentally different from that of the fuel that goes into the existing light-water reactor fleet.

At Crucible we believe that the future of supply chains is vertically integrated and

nuclear fuel presents a perfect case study on what happens when critical supply chains fragment - they grow vulnerable to exogenous shocks that are increasingly common, and break - a wave with everlasting ripple effects.

In this report we’ll break down the nuances of the nuclear fuel market in order to

identify the vulnerabilities we see and, consequentially, where we see the strongest

need for investment in today’s nuclear renaissance: onshore uranium enrichment and TRISO fuel fabrication.

The Nuclear Fuel Value Chain

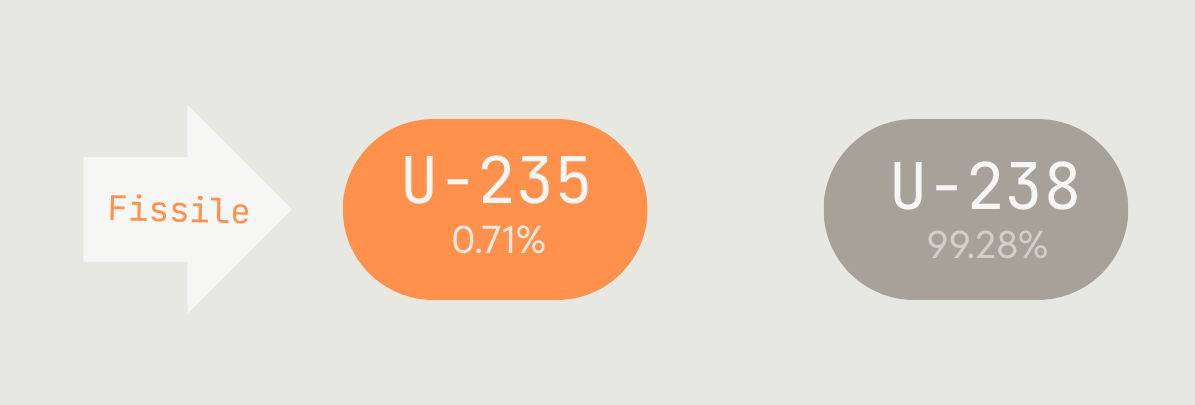

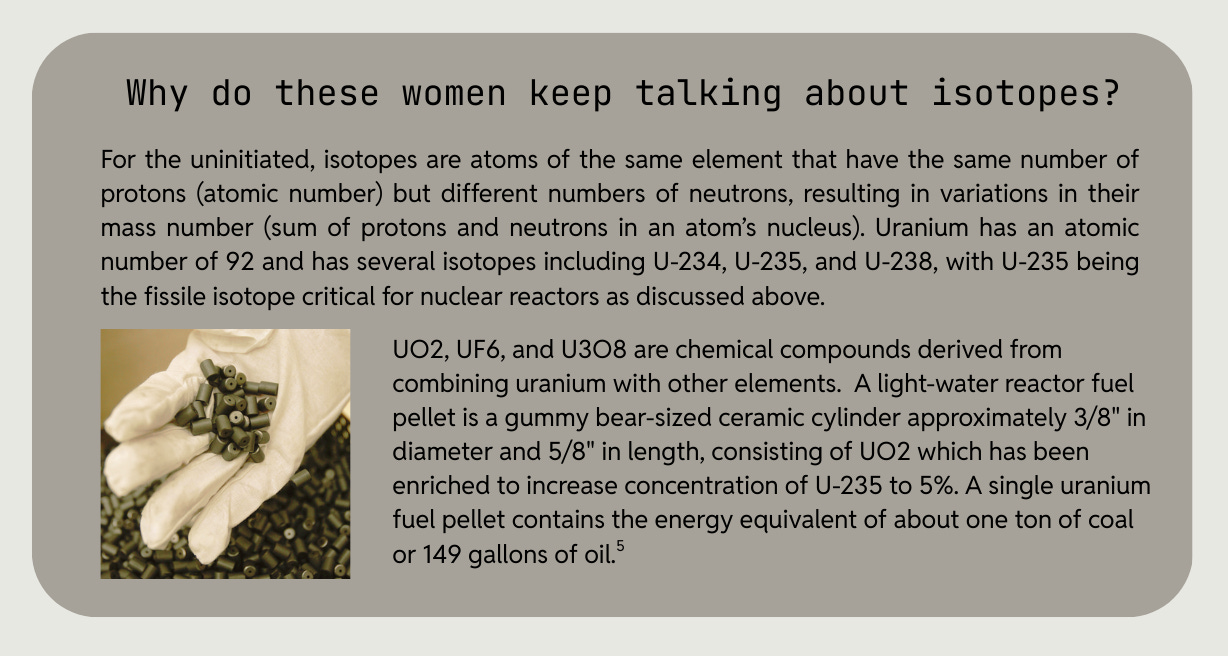

Let’s start with the nuclear fuel value chain - or the front end of the fuel cycle in nuclear jargon. Uranium primarily consists of two isotopes:

U-235 is the fissile isotope which can undergo nuclear fission, the process of splitting atoms that power nuclear reactors. The nuclear fuel value chain therefore focuses on increasing atomic concentration of U-235.

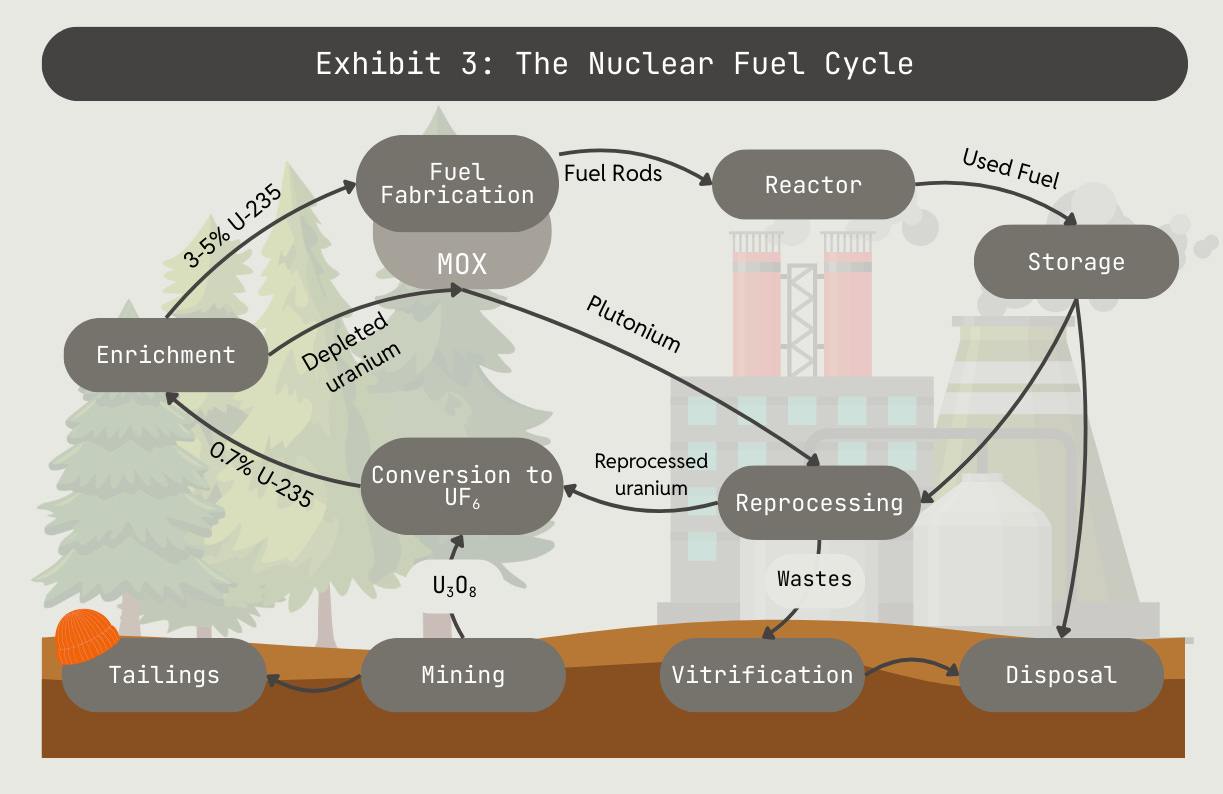

Mining: Uranium ore is mined and processed into yellowcake, which is mostly U-308 with various uranium oxides. We colloquially refer to this fuel as yellowcake or U3O8.

Conversion: Yellowcake is milled and then converted to uranium hexafluoride (UF6) for enrichment. UF6 is needed since it can be sublimated into a gas.

Enrichment: Enrichment increases the relative concentration of U-235 through gas centrifugation or laser isotope enrichment. Nuclear reactors consume two forms of enriched uranium: traditional light-water reactors (today’s fleet) consume low enriched uranium, or LEU, which has a maximum concentration of 5% U-235. Advanced reactors predominantly consume the aforementioned TRISO fuel composed of high-assay low enriched uranium, HALEU, which is 10%-20% U-235.

Fabrication: Enriched UF6 is deconverted back to an oxide form (UO2 or U3O8) to feed it into the fuel fabrication process. Traditional light-water reactors take that oxide powder and process it into fuel pellets and load it into rods. Advanced reactors use TRISO fuel particles instead - tiny ceramic coated uranium-bearing spheres designed to contain fission properties under extreme conditions.6 Aside from using the same deconverted uranium oxide, fabricating TRISO is an entirely unique process comprising acid dissolution, gelation, conversion, coating, and compaction. A minority of advanced reactors use metal fuel that require a yet different deconversion technology (transforming UF6 to uranium metal instead of oxide) and again a separate fabrication process. Our focus here is TRISO as the majority of advanced reactors rely on it.

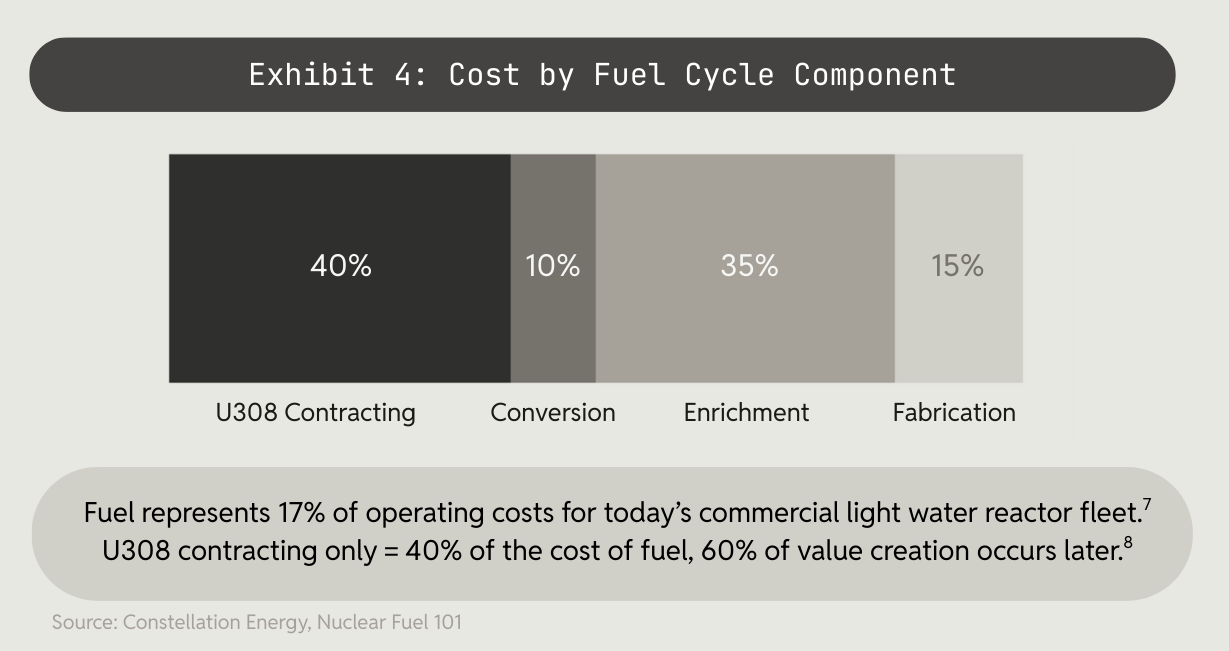

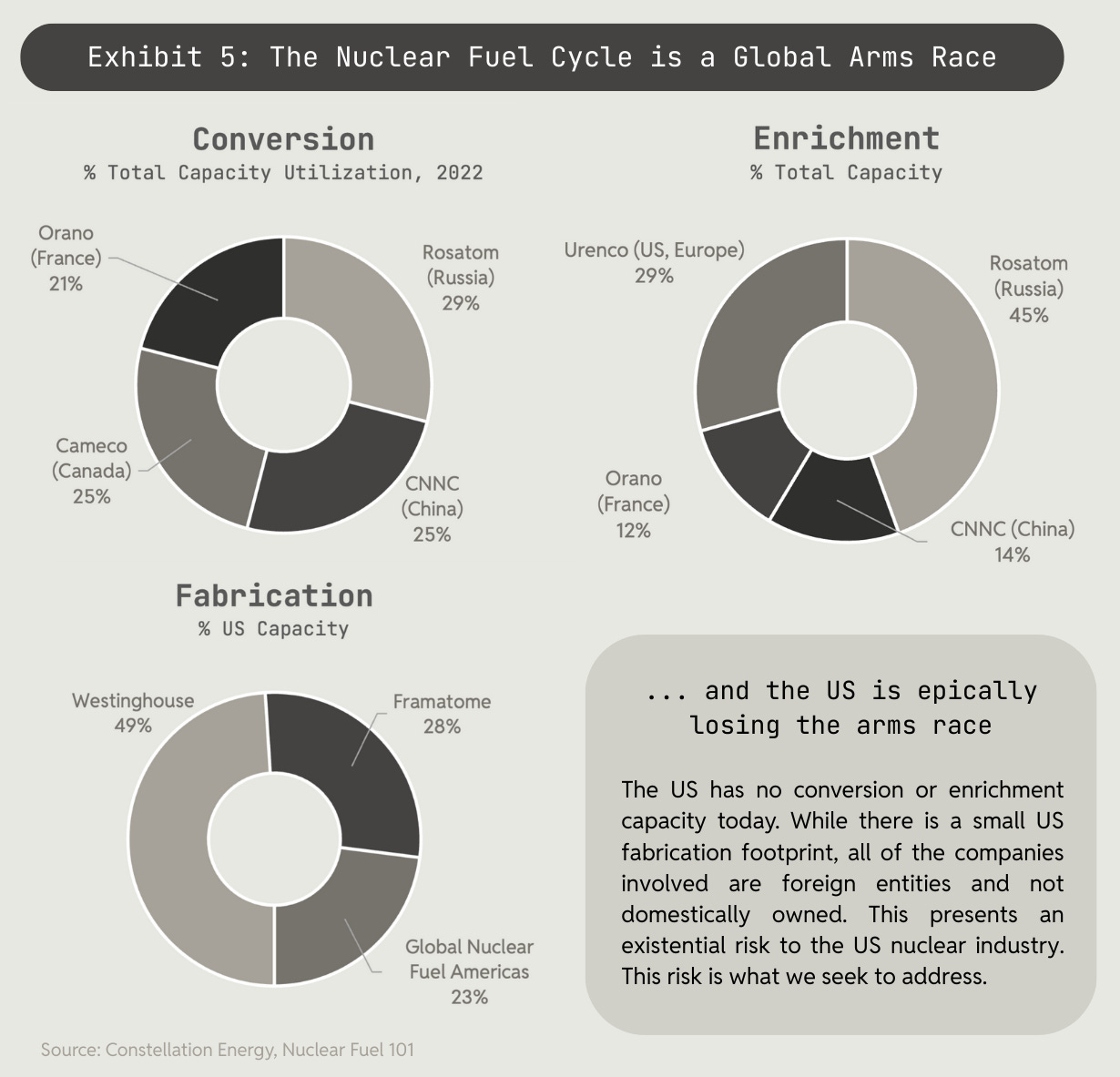

Nuclear fuel represents 17% of today’s light water fleet power plant costs. Yellowcake, conversion, and enrichment together comprise ~75% of the cost of fuel, and capital expenditure to build the plant accounts for 22% of the plant power cost. In short - traditional reactors require significant capital expenditure, but fuel cost on an ongoing basis is relatively low (the exact inverse of say natural gas turbines). The forthcoming generation of advanced reactors that will largely consume TRISO will mirror the cost structure of natural gas turbines, with comparatively lower capital expenditure and more expensive fuel. The fuel conversion to fabrication process accrues ~60% of the value for advanced reactors, but China and Russia dominate these stages.

U308 Market Dynamics

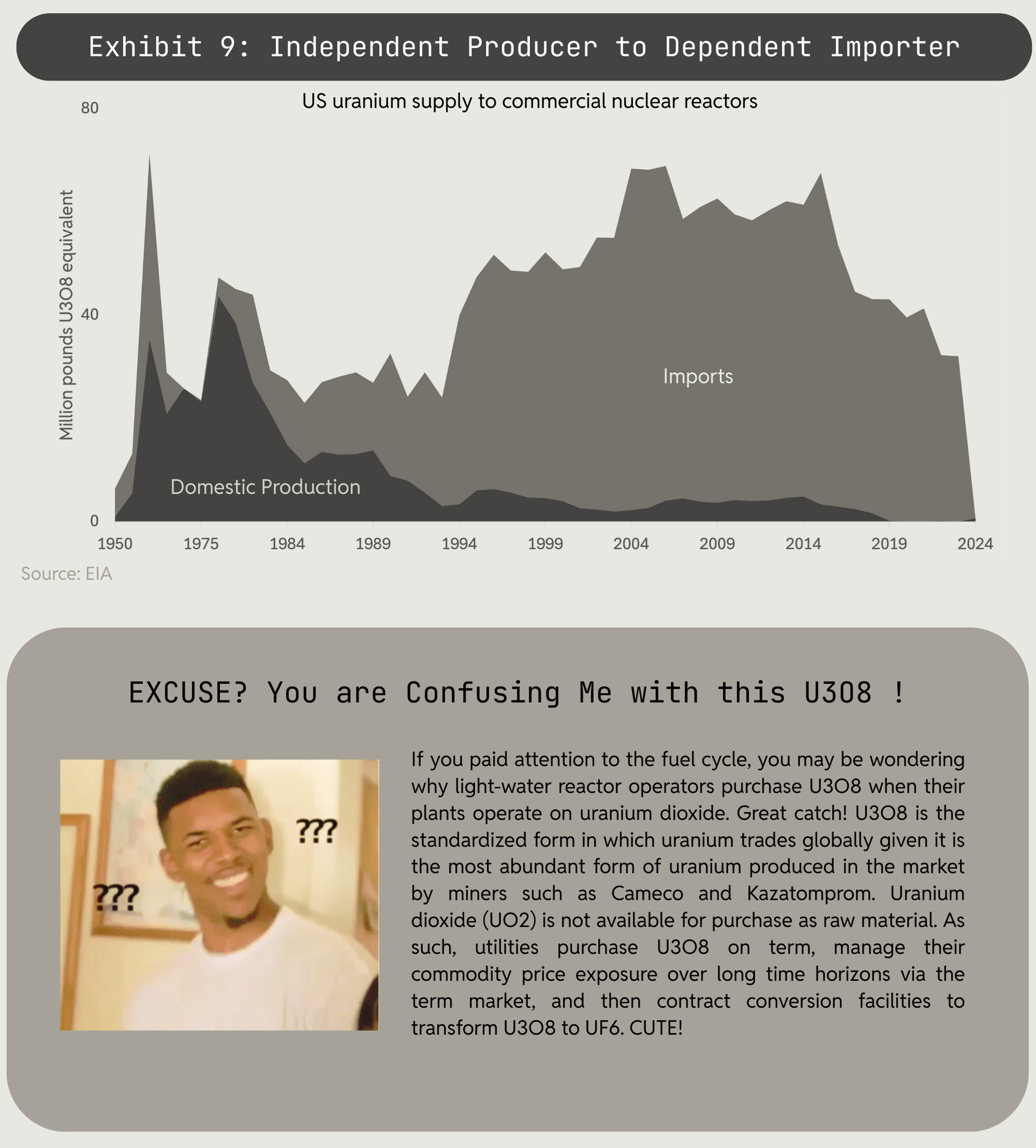

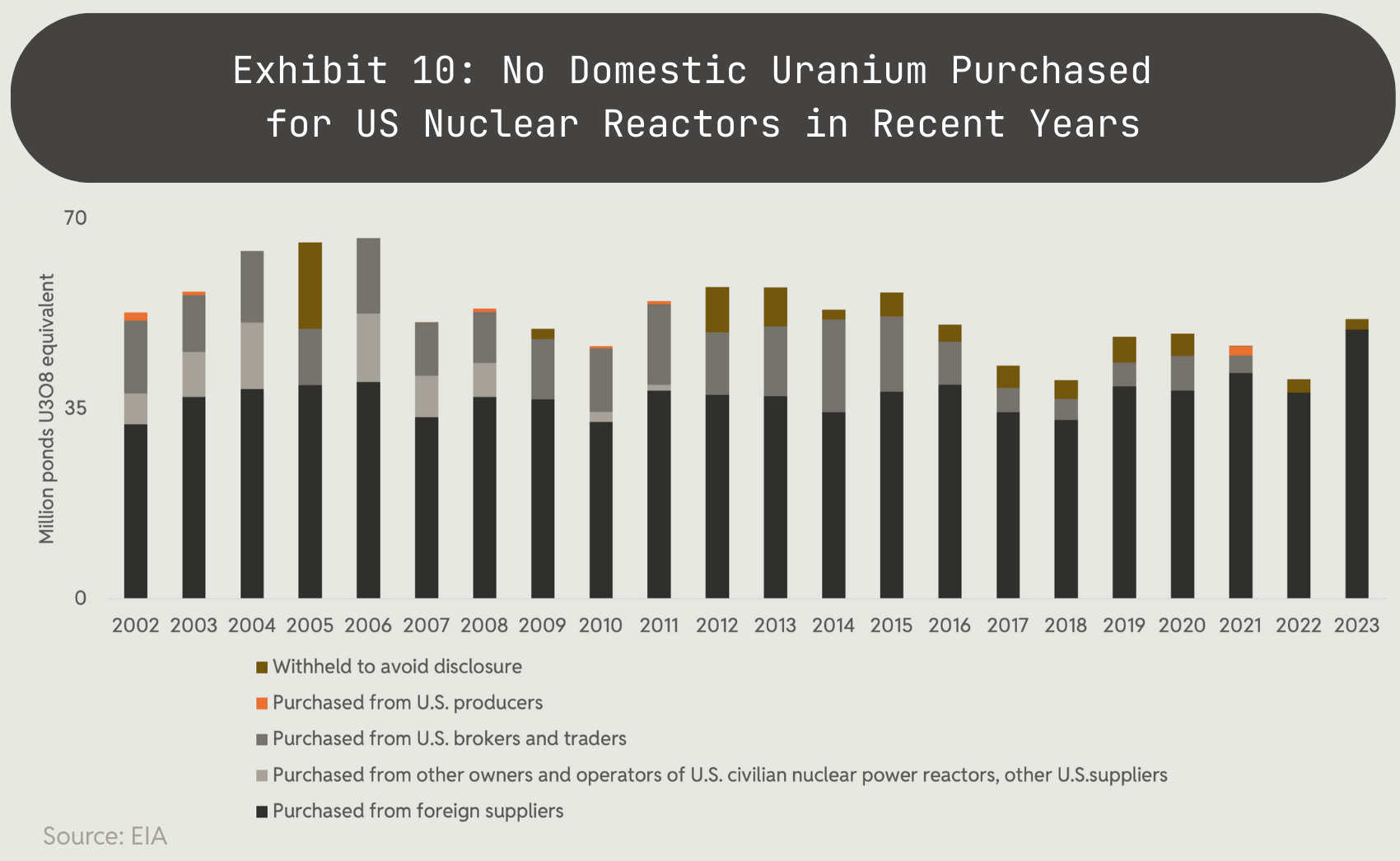

The US has devolved from self-sufficient production of its own U3O8 requirements in 1980 to producing negligible amounts today (Exhibit 9). This predicament is particularly concerning when looking at current U3O8 market structure. Most of the U3O8 market trades on termed, bilaterally negotiated contracts rather than spot market purchases. In other words, nuclear plant operators lock in the price and supply of fuel years in advance in a direct negotiation with a seller via bespoke agreements. Data shows 85% of U3O8 traded on term contracts in 2023, the last available datapoint. Market volume traded shows a 25% YoY decline in term contracting in 2024 from 160mm to 119mm pounds due to bans on Russian imports.

Meanwhile, the EIA reports that US nuclear power plants consumed 56 million pounds of U3O8 equivalent in 2022 - 37% more than the YoY decline in contracting. These datapoints illustrate that utilities are not contracting enough U3O8 to fill their ongoing requirements, let alone maintain an ongoing reserve buffer of 40-50% of their annual consumption, a historically standard practice.

Indeed, Cameco (the largest publicly traded uranium company by market cap and supplier of nuclear fuel) validates this: “Volume remains below replacement rate, this further increases the cumulative level of uncovered requirements in the decade to come, when primary supply is expected to be even more limited and uncertain, and secondary supply stacks have been drawn down.” Constellation Energy, the largest domestic reactor operator, also addresses the need to increase contracting in response to supply chain concerns in their December 2024 10-K filing: “Our most recent estimate of capital expenditures is approximately $3 billion and $3.5 billion for 2025 and 2026, respectively. Approximately 35% of projected capital expenditures are for the acquisition of nuclear fuel, which includes additional nuclear fuel to increase inventory levels in response to the potential for the continuing Russia and Ukraine conflict to impact our long-term nuclear fuel supply.” Constellation and nuclear operators broadly are now forced to dedicate significant amounts of capital expenditure to secure enough fuel to meet their reserves and compensate for the recently created reserve deficit.

Where utilities will source from and at what price are tricky questions: the US ban on Russian uranium imports, effective from August 11, 2024, has disrupted the U3O8 supply chain as Russia previously supplied about 20% of the US fleet’s fuel, and its retaliatory restrictions on enriched uranium exports to the US are even more detrimental. Waivers on the US’s ban are available until January 1, 2028, but they can’t be relied on.

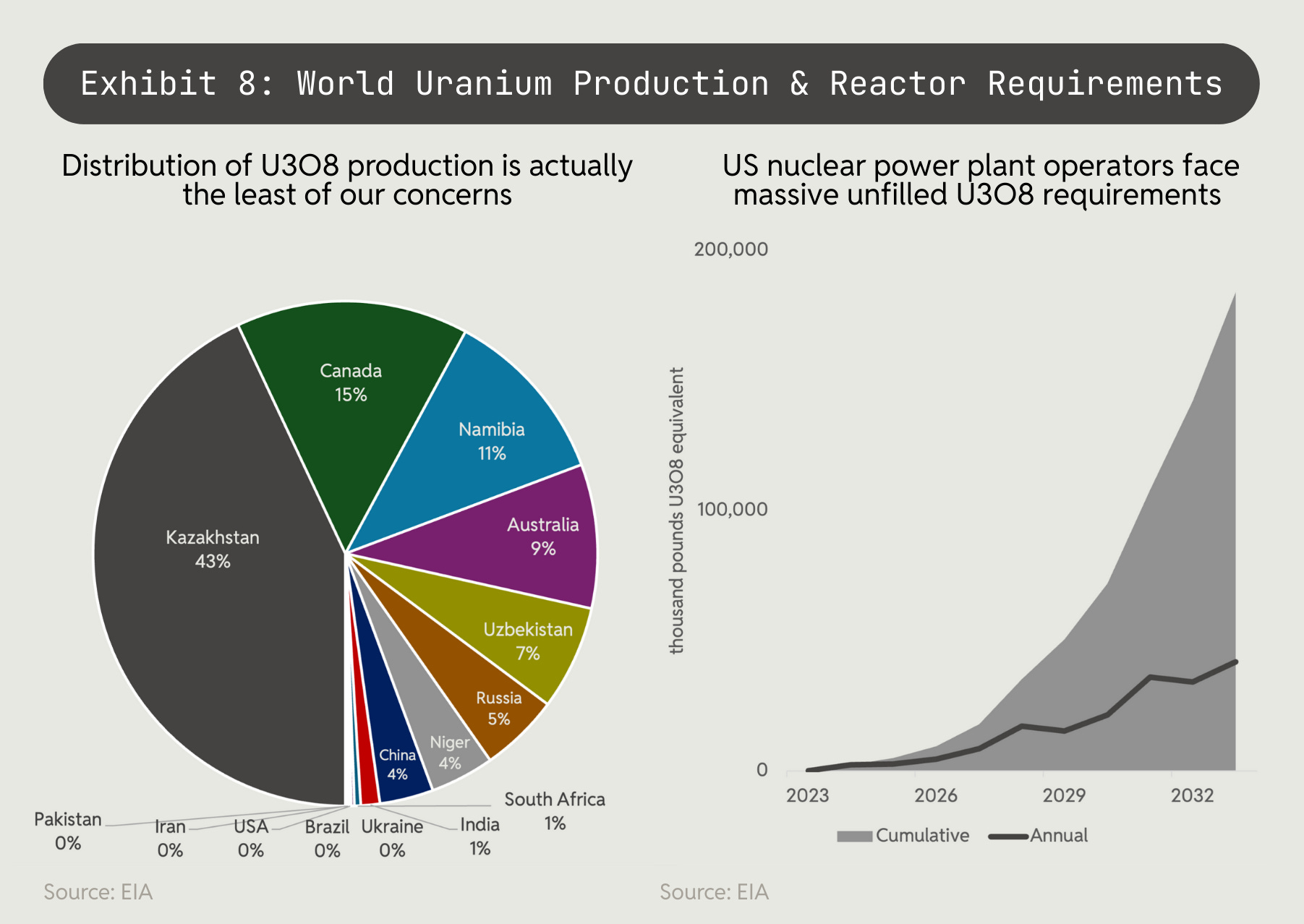

U3O8 supply concerns reach beyond Russia - supply chain challenges in Kazakhstan (world’s largest U3O8 exporter), the Russia-Ukraine war, and mine suspensions in Niger are all compounding forces straining the market. As always, markets alchemize to reflect current and future events. and these supply constraints have manifested in market pricing - term U3O8 average prices increased from $68/lb in December 2023 to $80/lb in March 2025.14 By the way - as U.S. utilities find themselves in a supply crunch for all of the above reasons, let us not forget the decline in share of domestic yellowcake supply:

The domestic utility U3O8 reserve deficit and increasingly tight supply-demand imbalance certainly raise concern, though the diversification of U3O8 production globally (95% of the global distribution of identified conventional resources are spread across 16 countries)15 relative to later fuel cycle stages (and the increased need for conversion, enrichment, and fabrication for advanced reactor fuel) should push national attention to later fuel cycle stages as first priority.

How U3O8 Trades and Clears

Spot U3O8 markets function dramatically different from other commodities markets with no exchange intermediaries or listed futures contracts available to transact. Pause to process that for a moment - no exchanges, no futures. The market functions as a true over the counter (OTC) market where prices are determined through negotiations between buyers (utilities) and sellers (global U3O8 miners).

Without an exchange, how does the market know the true price of the commodity? For now a handful of firms including TradeTech and UxC publish the price of U3O8 weekly by collecting contract terms from the market, calculating average prices, and publishing calculated averages weekly or monthly. Archaic really.

How do contract pricing and structuring actually work? Term contracts span between 3-15 years with deliveries starting one to three years after execution.16 The duration reflects the baseload nature of nuclear power and the need for security of supply. Contract pricing mechanics over this long duration vary - pricing can be fixed for the term, escalated by inflation (“base-escalated”), or variable based on the spot price at time of delivery - typically with embedded price floors and ceilings.17 Each pricing mechanism contains its own set of trade offs: base-escalated ensures some level of certainty while market based pricing introduces exposure to price volatility within the specified floor and ceiling, optimal for buyers who are structurally bearish on fuel prices.

We can’t help but draw a parallel here to the oil market, where spot oil traded bilaterally between participants from the industry’s inception in the mid-19th century until the establishment of futures and exchanges - most critically the NYMEX in the 1970s. The lack of an exchange exacerbated price volatility of the then scarce commodity undergoing its own identity crisis from lamp-enabler to automotive fuel to omnipresent in literally all materials worldwide.

All markets function better with more liquidity, and liquidity comes with standardized pricing, transparency, and market access. The sad, dysfunctional U3O8 markets can be used as a case study to both improve and build a more functional TRISO market, which Crucible will focus on in the coming years.

With an understanding of the fuel cycle and market dynamics of U3O8 established, we’ll continue to make our case on the shift to advanced nuclear and its fuel requirements presenting a dire need to repair this broken supply chain and the underlying market microstructure for both speculators and consumers alike.

Don’t be sad! You don’t need a token to not be sad.

Advanced Reactor Cost Benefit & Fuel Implications

Understanding why enrichment, conversion, and fabrication are increasingly important stages of the fuel cycle requires a quick understanding of the evolution of reactor designs and their respective fuel requirements, which we alluded to earlier but will expand upon here briefly. The current fleet of nuclear reactors predominantly consists of large (Gigawatt scale) light-water reactors (LWRs), while many of the reactor designs in development for future capacity are smaller (e.g. 30-300 Megawatts) and/or apply different cooling agent technologies (e.g. helium gas, liquid sodium, molten-salt, etc.).

As discussed, light-water reactors run predominantly on uranium fuel enriched up to 5% U-235. Advanced reactors, whose cooling agents can withstand higher temperatures (750 to 950°C) in order to deliver more cost-effective electricity, run on more concentrated fuel (i.e. higher U-235 enrichment). Most of these advanced reactors are inherently safe (a.k.a. passively safe) and target higher temperatures for enhanced generation efficiency. Inherently or passively safe signifies that the reactors do not incur damage and release radioactivity - even under extreme unforeseeable conditions (like the black swan earthquake and tsunami that led to the Fukushima incident) or human error and engineering systems failures (like the sequence that led to the Three-Mile Island incident). Advanced reactors rely on the laws of physics and natural phenomena to maintain safety. Pause to process the scientific wonder.

As such, and as a requirement to achieve their passive safety features, most of these reactors use TRISO fuel - designed to withstand extremely high temperatures with multiple ceramic coating layers that protect each uranium particle from releasing radioactivity. High-assay low-enriched uranium (HALEU) is a critical feedstock to manufacture TRISO (note: conventional light-water reactor fuel consumption consists of 5-10% HALEU too).

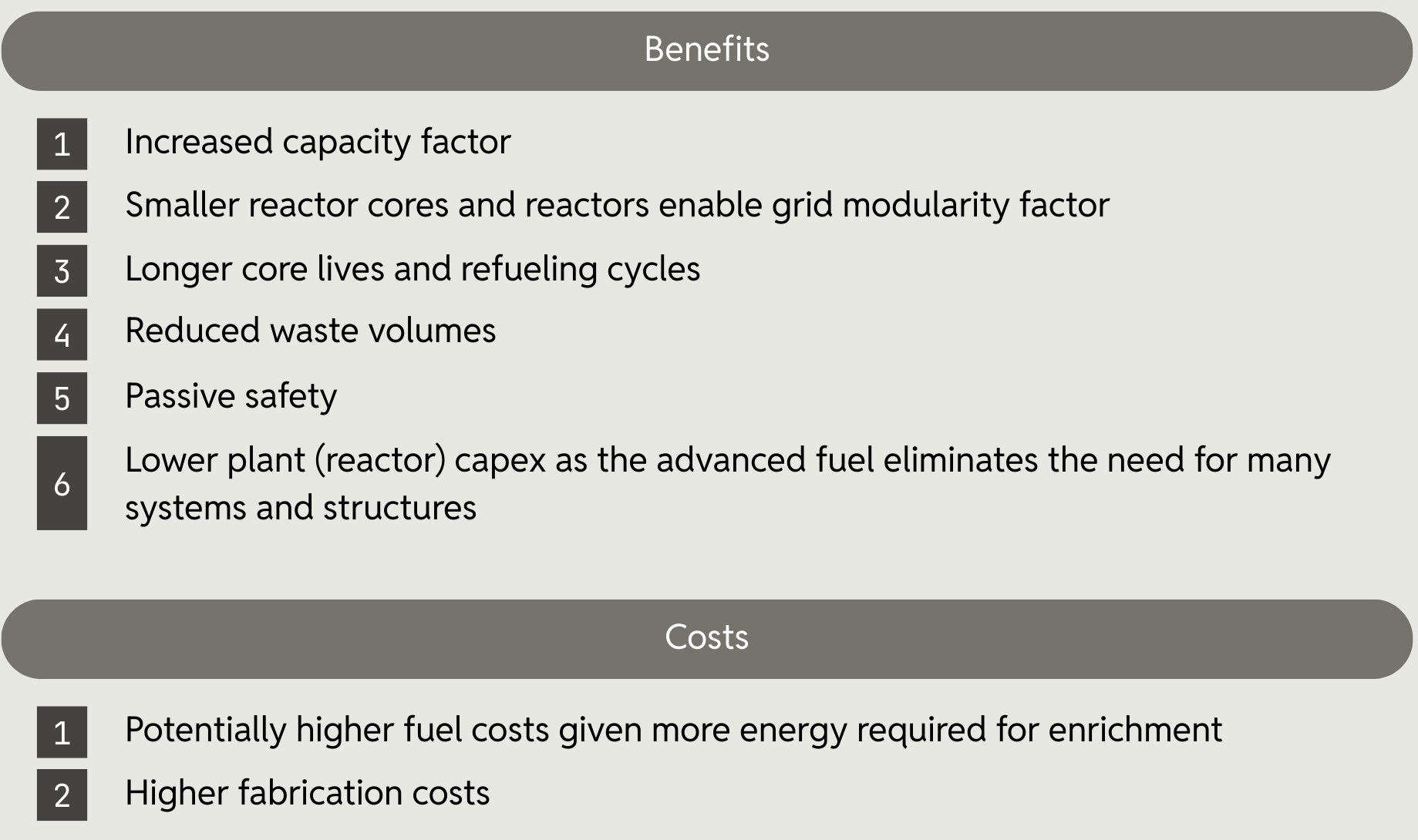

Let’s summarize the cost benefit of using advanced reactors with more potent fuel:

The benefits come at costs that are solvable with adequate focus on supply chains and deregulation. With an understanding of:

the front-end fuel cycle (with context on market structure and trading mechanics for the market structure nerds like us);

why shifting to advanced reactors makes sense, and;

the increased need for enrichment and fabrication that comes with advanced nuclear;

Let us now discuss the state of the union of enrichment and fabrication capacity globally.

Quick Rant on Why Metal Fuel Is Not Practical

Metal fuels are rods typically consisting of uranium metal alloys cast inside a steel tube and are used in fast spectrum reactors, where the neutrons have higher energy - totally distinct from light-water reactors and most salt or gas-cooled reactors). Metal fuels have been used in US DOE reactors in the past (EBR-I, EBR-II, FFTF), but those reactors have been shut down since the 1990s. Even then, the metal fuel was produced in the DOE complex as a commercial outfit to make metal fuel never existed even then - unlike TRISO fuel where General Atomics produced commercial amounts in the 1970s.

Metal fuel technology is at a much lower technology readiness level compared to TRISO and is a subject of R&D at US DOE labs today. No facilities exist today that can even remotely produce it at commercial scale or anything even remotely close. Idaho National Lab is leading technology development and has capabilities in the laboratory and R&D scale. TerraPower, a Bill Gates’ founded advanced reactor technology company, is working with General Electric to attempt to develop the manufacturing technology - but again, it’s low TRL.

Aside from manufacturing technology not being well-established, metal fuel producers need HALEU feedstock. We will address the HALEU supply chain in a moment - but - critically here metal fuel producers need metal HALEU! If you recall, HALEU is formed from enriched uranium in UF6 form which is deconverted into oxide that is then used in fuel fabrication for LWR fuel and TRISO fuel. But for metal fuel, it needs to be deconverted into metal. This requires its own technology that again does not exist in the US, exists in France and other places but not at commercial scale. We are practical here and thus focus on the technology we have now - TRISO fuel fabrication for advanced reactors.

The Sad State of Domestic Fuel Enrichment

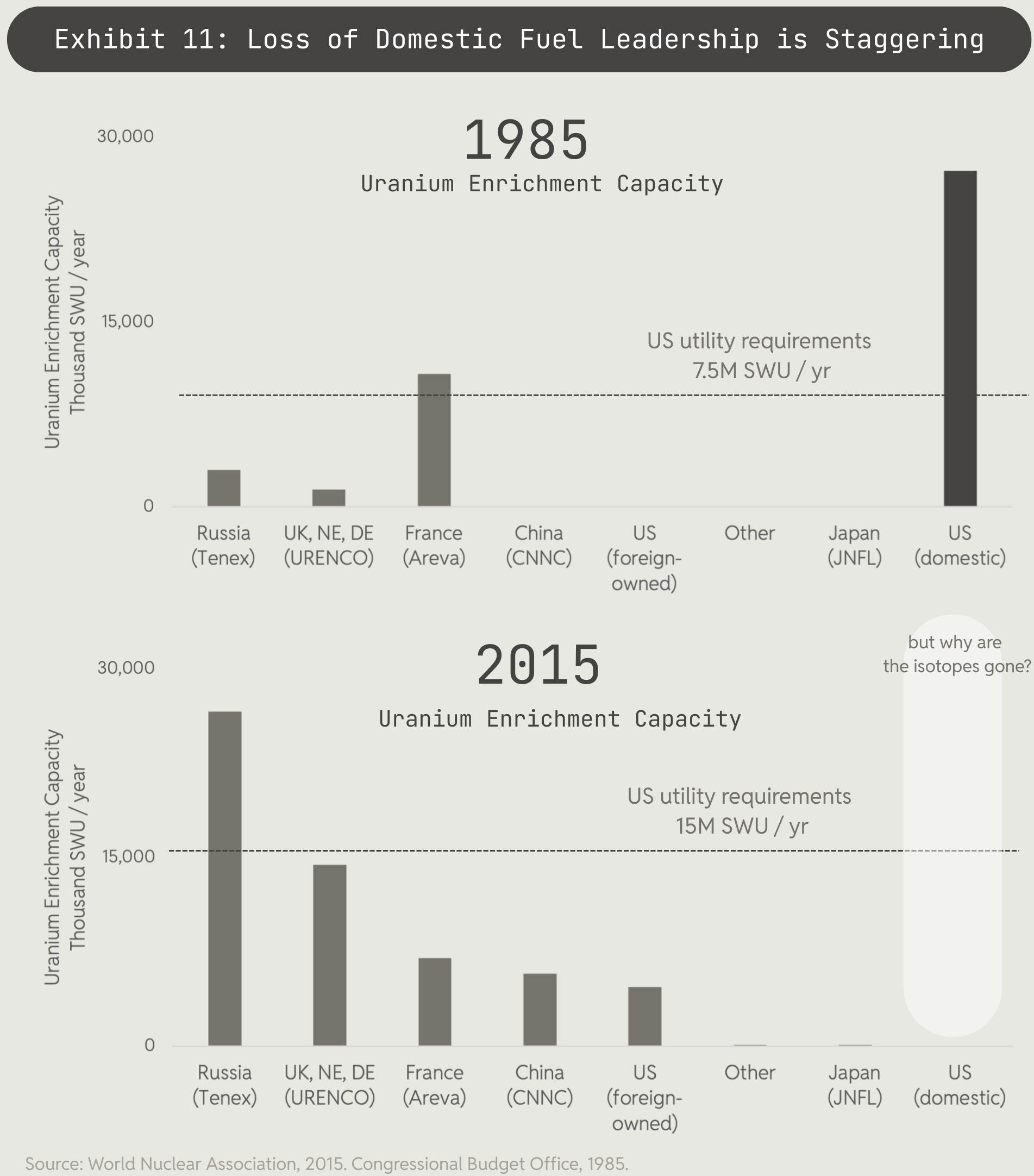

As most domestic advanced reactor designs ramp towards production around 2030, the supply chain for advanced fuel requires immediate attention. Russia dominates the supply chain that does exist today after the US gave away its own market leadership from 1985 onwards. Russia bears an enrichment capacity of 27.7 million SWU per year, comprising 46% of the world’s enrichment capacity, while the US bears zero capacity. Work units required for enriching isotopes are measured in separative work units, or “SWU” colloquially.

he US used to boast a comparable amount of SWU capacity in 1985, but now bears literally no enrichment capacity. We’ll discuss how this evolved in the next section. ASP Isotopes (ASPI), a South Africa based Nasdaq-listed company specializing in isotope enrichment, seeks to enter commercial production of HALEU to fill an MOU with Bill Gates’ TerraPower, who is paying the capital expense for the enrichment facility, in 2027. This will make ASPI one of, if not the only, sources of HALEU enrichment in the western hemisphere.

ASPI uses a laser-based enrichment technology that has proven powerful and successful in enrichment of another isotope already in commercial production - this technology outperforms traditional centrifuge technology used for enrichment in both performance and cost to impressive degrees. General Matter recently secured funding and a Peter Thiel board seat to enrich U-235 onshore as well, although there’s minimal information available on the company’s technology or deployment timeline. Additionally, existing participants are working to bring more SWU capacity to market near term. ASPI articulates the pressing need for HALEU as well as anyone: “Currently, there are no Western producers of HALEU in commercial quantities, and many SMR companies worldwide face substantial delays until this fuel supply issue is resolved. The Nuclear Energy Institute estimates that there may be a HALEU supply shortage of approximately 3,000 metric tons by 2035. However, based on discussions with and the interest received from potential customers, the Company believes this figure may be significantly larger.”

The DOE acknowledged the lack of Western enrichment capacity recently by committing an allocation of a domestic HALEU stockpile to five domestic nuclear developers to meet their near-term fuel needs. There is limited information on how much HALEU comprises the stockpile (we even asked someone who worked for the DOE), and the DOE’s specification that this allocation meets “near-term” needs is telling that stockpile reliance is not a sustainable solution. Further, the DOE states: “many advanced reactors will need HALEU to achieve smaller designs, longer operating cycles, and increased efficiencies over current technologies, but HALEU is not currently available from domestic suppliers.”

Own Goal (noun): the act of removing yourself from competition and letting your opponents win; i.e. burying yourself in your own grave.

Through the “Megaton to Megawatt” program, the US unwound its enrichment capacity and then went on to purchase half of our nuclear fuel requirements from Russia for the next... 20 years. In other words we derailed our own sovereignty over arguably the most critical fuel to mankind’s future and decided to pay Russia while letting China and Russia expand their capacity across generation, fuel, enrichment, and conversion.

Regs That Fu*ked Us

How did the United States cede leadership of fuel so important to national security to Russia? To no one’s surprise, overregulation hindered domestic producers’ ability to compete economically beginning in the 1970s. Please bear with us for a very brief but important regulatory discussion. Let us recount the ways that we fu*ked ourselves.

1970 - The National Environmental Policy Act (NEPA) | Requirement for detailed environmental impact assessments has significantly slowed the development and licensing of nuclear energy projects in the U.S. by increasing regulatory scrutiny and public involvement, often leading to delays and higher costs.

1978 - Uranium Mill Tailings Radiation Control Act (UMTRCA) | Set limits on radium in soil from mill tailings, increasing cleanup costs for producers.

1970 & 1985 - Clean Air Act | Restricted radon emissions, requiring costly impoundment systems for tailings. Post-1985 amendments tightened emission standards, further increasing compliance costs for operators.

1972 - Clean Water Act | Regulated runoff from mines, necessitating expensive treatment processes to protect water quality. The Act’s enforcement added layers of bureaucracy and cost, especially in water-scarce regions like the Southwest.

1976 - California bans new nuclear plant construction | No new construction until approval of a spent fuel disposal method, this rule is still in effect today.

1982 - Nuclear Waste Policy Act | Aimed to establish a permanent, underground repository for high-level radioactive waste and spent nuclear fuel by the mid-1990s. However, by the 1990s, the project was still in the planning and study phase, with no operational repository, which became a significant hurdle for plant operators as they stored spent fuel in temporary on-site facilities - increasing operational costs and regulatory burdens to comply with the stringent safety and environmental standards for on-site storage, without a long-term solution.

If you are sensing a theme - increasingly impractical rules increased operator costs and hindered development of domestic nuclear, a complete 180 from the development of nuclear energy under the US Government in 1945 as a result of the Manhattan Project. Beyond regulations, the Nuclear Regulatory Commission (NRC) plays a central role in licensing and overseeing uranium recovery operations under 10 CFR Part 40. While specific changes since 1985 are underdocumented, the NRC’s collaboration with the EPA illustrates a tightening of environmental standards over time. The NRDC has criticized these standards as inadequate, indicating ongoing tension between industry needs and regulatory protection.

While the United States regulated itself out of competition from the 1970s onwards, it then buried itself in its own grave in 1993 through execution of the “Megatons to Megawatts program” - a deal to purchase 500 tonnes of down-blended Russian high enriched uranium (into low enriched uranium, or LEU) from nuclear disarmament and military stockpiles over a 20-year period.

Through this deal, the US sourced approximately 50% of its nuclear fuel needs from Russia for 20 years until its completion in 2013. This influx of cheap Russian LEU reduced the economic incentive for maintaining domestic enrichment facilities, accelerating the decline in US production capacity across the fuel cycle.

Where does this all leave us today? Let’s summarize:

The US faces an estimated 60 GW power deficit in the next 5 years alone and needs to harness nuclear energy as a means to generate 24/7 reliable baseload, carbon-free electricity to compete in the global arms race for power and compute.

Advanced reactors will provide reliable, inherently safe baseload power and allow for modular grids as the nation ramps its power supply in the face of an aging and dysfunctional power grid. These reactors require advanced nuclear fuel (TRISO, and by derivative, HALEU).

After making existential regulatory missteps in the late 1900s, the US has negligible production capacity in any stage of the fuel cycle now - from mining to fabrication - with adversaries Russia and China dominating the later stages of the fuel cycle. China boasts the largest share of TRISO fabrication capacity in the world.

For now… we have some bullish tweets from think bois and our own DOE but it’s going to take a lot more than a tweet to bring back the American nuclear fuel industry.

The US Nuclear Renaissance Starts Now

What does this actually mean? As we alluded to in the intro, investment and attention are flowing into nuclear across a number of segments:

Advanced and Small Reactor Technology Startups: Companies such as Terrapower, X-energy, Oklo and Nuscale are a handful of many companies developing reactor prototypes as we speak. Prototypes are expected to be licensed and constructed by 2027 at the soonest, with expectations for construction to proliferate meaningfully in 2030 and beyond. Based on the value of publicly listed companies in this space and data on private investments, we estimate that $13.8bn has been invested in this sector of the renaissance, with Oklo and Nuscale accounting for $12bn and the balance attributed to private funding.

Extensions and Recommissioning of Large Scale Nuclear Plants: There are 93 reactors operational in the US now, representing 97 GW of capacity and accounting for just under 20% of US power generation. Five large scale reactors are up for license extension in 2025 to allow the reactors to continue operating for another 20 years in most cases, though potentially much longer. Palisades Nuclear Plant, an 800 MW plant in Michigan, is currently being recommissioned after shutting down in May 2022 and plans to restart by late 2025. Constellation Energy recently announced plans to recommission Pennsylvania’s 820 MW Three Mile Island Unit 1, which shut down in 2019, in order to fulfill a 20-year power purchase agreement with Microsoft. Beyond these two cases, there are few other (perhaps only one) reactors up for recommissioning. Reported costs for starting Palisades and Three Mile Island Unit 1 are $1.52bn and $1.6bn respectively, while costs to extend the life of active plants amounts to roughly $100-300m (between regulatory fees and safety upgrades).

Speculation: A palpable speculative frenzy around nuclear has taken hold as a derivative of compute and power narratives seizing markets, evidenced by Oklo’s (a pre-revenue SMR developer) 230% run in just 52 days between December 2024 and February 2025. As discussed before, yellowcake uranium lacks a futures market, and even liquid physical spot markets - thus speculation manifests itself across public equities - U3O8 miners, SMR developers (such as Oklo), companies developing enrichment technologies (ASP Isotopes, Centrus), the Sprott Physical Uranium Trust - which provides access to physical U3O8 - and ETFs comprised of all of the above. The total assets under management of publicly traded uranium investment vehicles in the US and Canada, including ETFs and trusts and companies mentioned above is estimated at $14.5bn as of year end 2024. This market has grown at an 87% CAGR between 2020 and 2024 - in large part driven by the launch of the Sprott Physical Uranium Trust and rising uranium prices in 2021.

But what about investments in the fuel? We are building cars, and ways to bet on the price of gasoline, for the future without considering that we need to procure gasoline. Oh, and the gasoline market is currently dominated by foreign adversaries.

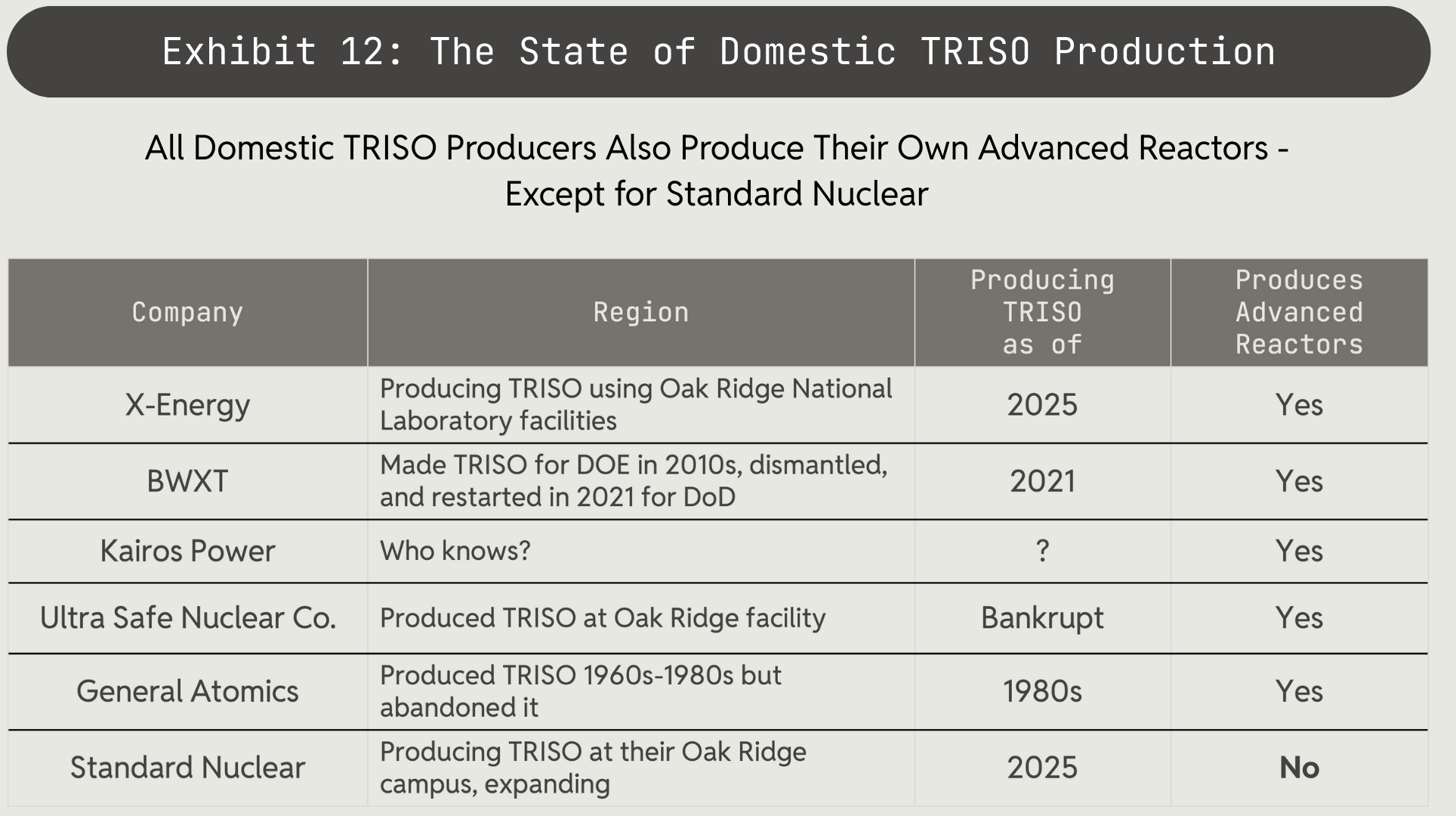

As we discussed, the US removed itself from the global chess board of enriched fuel suppliers over the course of the last 50 years. Recent efforts to re-enter TRISO production domestically have historically been packaged with advanced reactors - meaning even if investors were aware of the complexity of the TRISO fuel shortage and wanted to invest in onshore procurement, they couldn’t do this without also investing in said company’s advanced reactor technology too - an entirely different investment.

And let us be honest here - producing a nuclear plant is a tough business, evidenced by the bankruptcies of Ultra Safe Nuclear Corp. (USNC) and Westinghouse Electric Co.. While both faced their own unique challenges, to generalize: plant vendors face significant financial risks, namely cost overrun potential and an ongoing need to tap debt markets or fundraise to cover capital expenditure over lengthy construction times (hence X-Energy’s latest $700m fundraise). To draw another parallel to the oil industry, John D. Rockefeller focused his investment on the most lucrative and critical part of the value chain: oil refinement. In the same way, fuel fabrication and enrichment are demonstrably the most valuable parts of the nuclear supply chain - more so than ever for advanced reactors - but are chronically underinvested in today.

Standard Nuclear - America’s Nuclear Fuel Company

Standard Nuclear is building America's first advanced nuclear fuel company and is seeking to partner across the industry to provide TRISO fuel and make the KwH price of any compatible reactor type competitive.

As the country’s first and only independent TRISO fuel manufacturer without reactor development operations of its own, Standard Nuclear’s model strengthens the advanced reactor supply chain by providing a reliable, independent source of fuel. Standard Nuclear owns and operates a set of fully equipped commercial-scale facilities totaling 19,000 square feet on its 36.8 acre campus located at the former K-25 Nuclear site in Oak Ridge, TN. The Company operates its fully permitted radiological facilities to manufacture and supply TRISO fuel forms with varying specifications for its multiple commercial and government customers.

Founded in 2024, the company has booked $5 million in contracts in the first quarter of 2025, and signed a major fuel offtake agreement for over 1 MTU of fuel with an additional 1.5 MTU in negotiation, representing more than $100 million in non-binding fuel sales for 2027. In just a few months, the company has established strategic customer relationships for its various products and services with a diversified group of commercial and government customers including NASA, Radiant Industries, Antares, Nano Nuclear Energy, The U.S. Department of Energy National Laboratories, and the Department of Defense. Through these efforts, it is helping to eliminate U.S. reliance on geopolitical adversaries for these strategically vital technologies. Let’s rip.

Conclusion

The time to invest in the domestic nuclear fuel supply chain is… 1970?

We simply can’t, as a country, continue to depend on adversaries for fuel critical to national security, in particular at a time when power infrastructure investment is mandatory and geopolitical dynamics are shifting towards multipolarity. We want to see all stages of the nuclear fuel cycle move back onshore - from mining to fabrication - and we see the strongest need to focus on enrichment and fabrication given the stronghold Russia and China hold and the relative value accrual of these stages.

More broadly, we believe that the future of supply chains - from fuel, to semiconductors, to quantum materials - is vertically integrated, and nuclear fuel presents a perfect case study on what happens when supply chains fragment: the supply chain becomes vulnerable to exogenous events that are increasingly more common (trade wars, physical wars) and markets in the supply chain become higher friction, inefficient and in nuclear’s case borderline inaccessible - evidenced by the lack of HALEU enrichment and TRISO fabrication in the western hemisphere and the precarious predicament domestic utilities face in procuring both U3O8 and enriched fuel alike.

Our team at Crucible is taking the first step by backing Standard Nuclear to drive domestic TRISO fabrication for all compatible advanced reactors. We are keeping a close eye on ASP Isotopes and General Matter and their forthcoming expansion of HALEU enrichment in the western hemisphere. Having spent over a decade building the foundations of the Bitcoin industry and the markets and infrastructure that support it, we are actively looking for opportunities to help find, fund, and develop the market structure needed to establish nuclear fuels as an active commodity market. Our door is always open for collaboration.

Merci Mon Ami

We are not nuclear physicists. We are three women with a Bloomberg terminal. The below individuals were instrumental in the writing of this report:

Thomas Hendrix, GP, Decisive Point. Chairman, Standard Nuclear: Tommy, you’re one of a kind. Thanks for letting us be a part of the Standard Nuclear journey.

Dan Stout, Founder, Advanced Nuclear Advisors: his perspective on US nuclear regulation is unmatched.

Mike Alkin, CIO, Sachem Cove: we haven’t met yet but his work on U3O8 market structure sparked the fire that is our pursuit to repair fuel markets.

Daniel Yergin, Author, The Prize: his perspective on the history of the oil markets and the 20th century is foundational to our view of commodities markets and the future of nuclear fuel markets.

Jacob Rowe, Founder, Rogue Funds: for his ongoing collaboration and thoughtful research on isotope enrichment.

Drew Armstrong, COO, Cathedra Bitcoin: for introducing me to Isodope (Isabelle Boemeke we love you) in 2021 and letting me drag him to a Diablo Canyon protest in 2023.

Sources & Citations

Citations

Department of Energy. https://liftoff.energy.gov/wp-content/uploads/2023/03/20230320-Liftoff-Advanced-Nuclear-vPUB.pdf.

Net Zero Tracker. https://zerotracker.net/.

Department of Energy. https://www.energy.gov/articles/cop28-countries-launch-declaration-triple-nuclear-energy-capacity-2050-recognizing-key.

Department of Energy. https://liftoff.energy.gov/wp-content/uploads/2023/03/20230320-Liftoff-Advanced-Nuclear-vPUB.pdf.

Isodope. https://isodope.com/blog/density-of-uranium-why-nuclear-is-so-powerful/.

Department of Energy. https://www.energy.gov/ne/articles/triso-particles-most-robust-nuclear-fuel-earth.

Nuclear Energy Institute. https://www.nei.org/resources/reports-briefs/nuclear-costs-in-context.

Constellation Energy. https://investors.constellationenergy.com/static-files/200ef852-8674-4595-8cdf-80d06ea20c60.

Energy Information Adminstration. https://www.eia.gov/uranium/marketing/pdf/2023%20UMAR.pdf.

Cameco. https://www.cameco.com/invest/markets/supply-demand.

Energy Information Adminstration. https://www.eia.gov/uranium/marketing/pdf/2023%20UMAR.pdf.

Cameco. https://www.cameco.com/invest/markets/supply-demand.

Constellation Energy. https://last10k.com/sec-filings/ceg/0001868275-25-000023.htm.

UxC. https://www.uxc.com/p/prices/UxCPrices.aspx?currency=eur.

Energy Information Adminstration. https://www.eia.gov/uranium/marketing/pdf/2023%20UMAR.pdf.

World Nuclear. https://world-nuclear.org/information-library/nuclear-fuel-cycle/uranium-resources/uranium-markets.

Uranium Info. https://www.uranium.info/contract_pricing_overview.php.

Department of Energy. https://www.energy.gov/ne/articles/triso-particles-most-robust-nuclear-fuel-earth.

Energy Information Adminstration. https://www.eia.gov/uranium/marketing/table16.php.

ASP Isotopes. https://ir.aspisotopes.com/news-events/press-releases/detail/58/asp-isotopes-inc-completes-commissioning-of-first-quantum.

Department of Energy. https://www.energy.gov/articles/us-department-energy-distribute-first-amounts-haleu-us-advanced-reactor-developers.

Department of Energy. https://www.energy.gov/em/moab/overview-moab-umtra-project.

Environmental Protection Agency. https://www.epa.gov/radtown/radioactive-waste-uranium-mining-and-milling.

Environmental Protection Agency. https://www.epa.gov/radtown/radioactive-waste-uranium-mining-and-milling.

California Legislative Analyst's Office. https://lao.ca.gov/BallotAnalysis/Initiative/2015-001.

Environmental Protection Agency. https://www.epa.gov/laws-regulations/summary-nuclear-waste-policy-act.

Natural Resources Defense Counsil. https://www.nrdc.org/bio/geoffrey-h-fettus/nrc-moves-entrench-dreadful-uranium-mining-standards.

Exhibits

JP Morgan via OWID. Heliocentrism by Michael Cembalest.

Morgan Stanley. 2025 Outlook: Chasing Growth.

A Crucible original, she cute tho. Stevesy easter egg anyone?

Constellation Energy. Nuclear 101. https://investors.constellationenergy.com/static-files/200ef852-8674-4595-8cdf-80d06ea20c60.

Constellation Energy. Nuclear 101. https://investors.constellationenergy.com/static-files/200ef852-8674-4595-8cdf-80d06ea20c60.

Cameco. Supply & Demand. https://www.cameco.com/invest/markets/supply-demand.

Energy Information Association. 2023 Uranium Marketing Annual Report. https://www.eia.gov/uranium/marketing/pdf/2023%20UMAR.pdf.

World Nuclear. World Uranium Mining Production. https://world-nuclear.org/information-library/nuclear-fuel-cycle/mining-of-uranium/world-uranium-mining-production.

Energy Information Association. Morgan Stanley EIA.

Energy Information Association. 2023 Uranium Marketing Annual Report. https://www.eia.gov/uranium/marketing/pdf/2023%20UMAR.pdf.

Centrus Energy. Fueling the Future of Nuclear Power. https://www.nationalacademies.org/documents/embed/link/LF2255DA3DD1C41C0A42D3BEF0989ACAECE3053A6A9B/file/DA93741315D0824C625902A954318F9EBDE58A25C58E?noSaveAs=1.

Crucible Capital proprietary research

Or just build out our supply of proven 6% enriched fuel and save the world with standard American nuclear.

Are the VCs actually destroying lowest-cost American nuclear? Sometimes it feels like it